Why NRIs Should Invest in Liquid Funds?

Read More

_1769861757488.webp&w=3840&q=75)

For millions of Indians, the National Pension System (NPS) has been a preferred tool for retirement planning. Considering this, with the introduction of the NPS Vatsalya Scheme on 18 September 2024, NRIs can now participate in a retirement plan and plan a stable financial future for their children in India. This scheme is available to all minor children. Additionally, once the child turns 18, the amount can be withdrawn or transferred to an NPS account, subject to conditions.

Further, want to know more about the NPS Vatsalya scheme? Read the blog and get all the information about the scheme and its eligibility, benefits, opening process, and more.

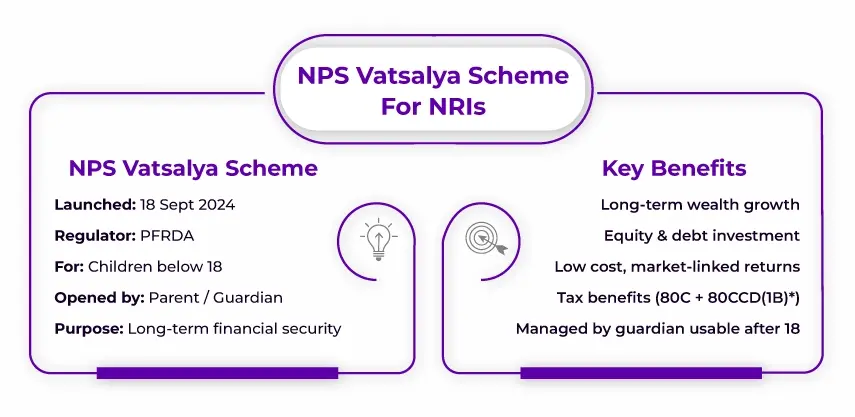

NPS Vatsalya Scheme was launched on 18 September 2024 under the National Pension System (NPS). It is a specifically designed pension scheme that allows parents and guardians to open an account for minors. This scheme is administered and regulated by the Pension Fund Regulatory Authority of India (PFRDA).

With this scheme, NRIs can contribute towards the future of their children. It provides a disciplined investment method to investors that leads to the accumulation of significant wealth over time.

Further, let's know the key highlights of the NPS Vatsalya Scheme.

| Particulars | Details |

|---|---|

| Scheme | NPS Vatsalya Scheme is a subset of NPS and is regulated by PFRDA. |

| Eligibility | All minor Indian citizens under 18 years of age are eligible for this scheme. |

| Account Operator | Only parents have permission to open, deposit, or withdraw funds from the accounts. |

| Account Beneficiary | Only minor children can be the beneficiary. |

| Minimum Contribution Limit |

The minimum contribution limit for account opening is INR 1,000 p.a. |

| Maximum Contribution Limit | There is no maximum contribution limit in the NPS Vatsalya scheme. |

| Interest Rate | The interest rate of NPS is between 9.5% to 10%. |

| Tax Benefits |

|

This was all about the NPS Vatsalya scheme. Moving ahead, let' whether NRIs can invest in this scheme or not.

Yes, NRIs can invest in the NPS Vatsalya scheme; however, for this, they need to fulfill certain conditions. These are as follows:

Further, the parent or legal guardian of the children, whether living in India or overseas, on behalf of the children, can open an NPS Vatsalya scheme. Several platforms allow NRIs to open and manage their NPS Vatsalya accounts from anywhere in the world at anytime.

So, yes, from the above information, it is clear that NRIs can invest in the NPS Vatsalya scheme. Moving further, let's know the features of the NPS Vatsalya scheme.

The following are the features of the NPS Vatsalya scheme:

These were the key features of the NPS Vatsalya scheme. Moving ahead, let's know the eligibility criteria for the NPS Vatsalya scheme.

The following people are eligible for the NPS Vatsalya scheme:

These were the eligibility criteria that you need to consider before applying for the NPS Vatsalya scheme. Moving ahead, let's now look at the documents required for NRI/ OCIs for this scheme.

Here is the list of documents required to open an NPS Vatsalya Scheme:

These are the documents required for NRI/ OCIs to open an NPS Vatsalya scheme. Moving further, how to open an NPS Vatsalya account.

Using the eNPS website or through Points of Presence (POPs), which include major banks, India Post, Pension Funds, etc, parents and guardians can open the NPS Vatsalya scheme. Here are the steps that you need to follow:

So this is how you can open an NPS Vatsalya scheme. Moving ahead, let's know the contribution, withdrawal, and exit rules of the NPS Vatsalya scheme.

NPS Vatsalya Scheme, before the child turns 18 years old, offers partial withdrawal. Here are the following conditions under which you can apply for a partial withdrawal from the NPS Vatsalya account:

Once the child turns 18, you can convert the NPS Vatsalya scheme into a regular NPS account, which the child can manage independently. However, after turning 18, the child within 3 months needs to do a fresh KYC. The accrued contribution amount stated in the NPS Vatsalya account will be transferred to the standard NPS account.

Additionally, the child can also opt for exit from the NPS Vatsalya scheme instead of converting it to a Standard NPS account when they turn 18. Further, in case of an unfortunate death, the rules of the NPS Vatsalya scheme are as follows:

These were the contribution, withdrawal, and exit rules of the NPS Vatsalya Scheme. Moving further, now let's know about the benefits of this scheme for NRIs.

Here are some of the key benefits of the NPS Vatsalya scheme for NRIs:

These were the key benefits of the NPS Vatsalya scheme for NRIs and how it helps them in growing their income for fulfilling future financial needs of their children.

Lastly, to secure the future of their child, the NPS Vatsalya scheme for NRIs is an excellent investment opportunity. This scheme is a tax-efficient and disciplined investment approach.

Further, with Savetaxs, the NPS Vatsalya scheme process becomes seamless, certifying a well-planned financial future for your children. So, if you are an NRI who wants to build a secure financial foundation for your child in India, connect with us and choose the right investment option as per your investment goals, time horizon, and risk appetite.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr Shaw brings 8 years of experience in auditing and taxation. He has a deep understanding of disciplinary regulations and delivers comprehensive auditing services to businesses and individuals. From financial auditing to tax planning, risk assessment, and financial reporting. Mr Shaw's expertise is impeccable.

Want to read more? Explore Blogs