What is the Difference Between SWIFT Code and IFSC Code?

Read More

An NRI recurring deposit account is a savings instrument for NRIs in which they deposit a fixed amount each month over a chosen tenure, ranging from 6 months to 10 years, subject to bank-specific policies. The funds deposited in the account earn interest, and the entire corpus generated over the tenure is paid to the investor upon the account's tenure ending.

NRIs looking to build a consistent savings habit in India should consider an NRI RD account, as it is a safe and secure option. Similar to regular NRI FDs, an NRI recurring deposit account lets you earn good interest over a specified tenure with minimal risk and assured returns.

In this blog, we will explore every aspect of NRI RD accounts, including benefits, types, opening an NRI recurring deposit account, account taxation, and more.

A recurring deposit for NRIs is a secure savings instrument where a non-resident indian will deposit a fixed sum of money every month for a specific time period. Over time, the deposit funds earn interest, and at the end of the term, the corpus built over the year is paid back to the account holders.

NRIs prefer recurring deposits as the process is simple to understand, it carries low risk, and it helps you build a consistent saving habit.

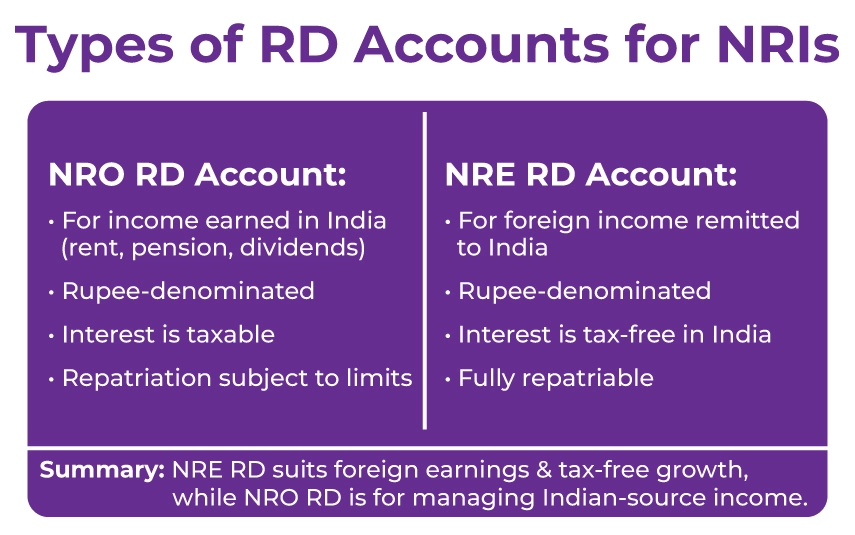

Now that we know what a recurring deposit for NRIs is. Let us understand the two types of NRI RD accounts.

An NRO RD account is appropriate for NRIs with income sources in India, such as pensions, rent, or dividends. This account is an indian ruppe denominated account, and the interest you earn on this account is taxable. The interest rates of NRO RD accounts may vary from bank to bank.

An NRE RD account is suitable for NRIs who earn in foreign currency but are likely to deposit the money in India to build a long-term corpus. Similar to an NRO RD account, an NRE RD account is also an Indian rupee-denominated account, and the interest earned on it is tax-free in India. Additionally, the funds are easily repatriable without restrictions.

In a nutshell, NRE RD accounts allow NRIs to securely park their foreign earnings in India, earn tax-free interest, and build a corpus over time, with no risk, attractive returns, and currency appreciation benefits.

Savetaxs helps you open an NRI banking account online from anywhere in the world.

The following are some of the key features of an NRI recurring deposit account:

Fixed Monthly Deposits: NRI investors must deposit a predetermined monthly amount into the account for the chosen tenure.

Interest: Both NRE and NRO RDs offer interest, and the rate varies from one financial institution or bank to another.

Fixed Returns: The returns are fixed in recurring deposit accounts, as the interest rate is predetermined when you open an RD account.

Taxation: The taxation obligations of NRI RD accounts are as follows: NRE RDs are exempt from tax in India, whereas NRO RDs are taxable, and the interest generated is liable to tax under the current Income Tax laws.

Repatrition: The NRE RD account allows full repatriation without restrictions, subject to FEMA guidelines, unlike an NRO RD account, which has limited repatriation.

| Bank Name | Regular NRI RD Interest Rate (p.a.) | Senior Citizen Interest Rate (p.a.) | Tenure Range |

|---|---|---|---|

| State Bank of India (SBI) | 6.50% – 7.00% | 7.00% – 7.50% |

6 months – 10 years

|

| Bank of Baroda | 6.25% – 7.00% | 6.75% – 7.50% |

6 months – 10 years

|

| Punjab National Bank (PNB) | 6.50% – 7.25% | 7.00% – 7.75% |

6 months – 10 years

|

| Canara Bank | 6.50% – 7.25% | 7.00% – 7.75% |

6 months – 10 years

|

| Union Bank of India | 6.50% – 7.25% | 7.00% – 7.75% |

6 months – 10 years

|

| Indian Bank | 6.25% – 7.10% | 6.75% – 7.60% |

6 months – 10 years

|

| HDFC Bank | 7.00% – 7.50% | 7.50% – 8.00% |

6 months – 10 years

|

| ICICI Bank | 7.00% – 7.40% | 7.50% – 7.90% |

6 months – 10 years

|

| Axis Bank | 7.00% – 7.50% | 7.50% – 8.00% |

6 months – 10 years

|

| Kotak Mahindra Bank | 7.20% – 7.60% | 7.70% – 8.10% |

6 months – 10 years

|

| IDFC First Bank | 7.00% – 7.75% | 7.50% – 8.25% |

6 months – 10 years

|

| Yes Bank | 7.25% – 7.75% | 7.75% – 8.25% |

6 months – 10 years

|

| Federal Bank | 7.10% – 7.75% | 7.60% – 8.25% |

6 months – 10 years

|

| RBL Bank | 7.30% – 7.80% | 7.80% – 8.30% |

6 months – 10 years

|

| IndusInd Bank | 7.25% – 7.75% | 7.75% – 8.25% |

6 months – 10 years

|

| AU Small Finance Bank | 8.00% – 8.25% | 8.50% – 8.75% |

6 months – 10 years

|

| Ujjivan Small Finance Bank | 8.25% – 8.75% | 8.75% – 9.25% |

6 months – 10 years

|

| Equitas Small Finance Bank | 8.00% – 8.50% | 8.50% – 9.00% |

6 months – 10 years

|

| Jana Small Finance Bank | 8.10% – 8.60% | 8.60% – 9.10% |

6 months – 10 years

|

| Suryoday Small Finance Bank | 8.20% – 8.65% | 8.70% – 9.15% |

6 months – 10 years

|

Note:Interest rates shown are indicative and subject to change based on bank policies and tenure. Please verify the latest rates with the respective bank before investing.

The following are the steps that NRIs must follow to open an NRI RD account:

The tax treatment of the NRI RD account differs significantly based on the type of NRI RD account you hold.

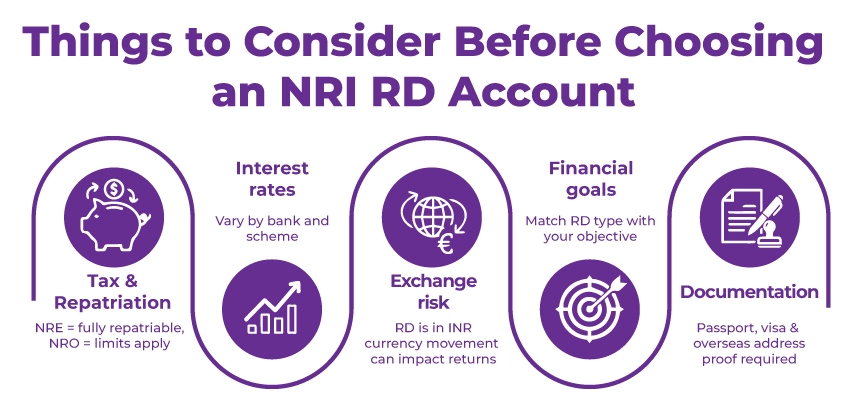

The following are key points NRI must keep in mind before selecting an NRI RD account for itself.

Repatriation and tax rules: Before choosing any one out of the two accounts, you must know the repatriation rules and the tax treatment of the account in and out. As NRE RDs are completely repatriable, whereas an NRO RD for NRI account has set repatriation limits.

Please ensure that the taxation and repatriation laws are subject to change in accordance with the directions issued by the Reserve Bank of India & The Foreign Exchange Management Act (FEMA).

Interest Rate Variations: The NRI RD interest rates depend on the financial interest rate or the account with which you have opened the account.

Exchange Rate Risk: RD account funds are held in INR; changes in currency values or exchange rates may affect the potential gains upon conversion back to foreign currency.

Financial Goal: When choosing an NRI RD account, consider your financial objective and select the account that best aligns with your needs.

Documentation: As an NRI, you must provide all required documents, such as your identity proof, visa, and overseas proof, to make the account opening process easier.

As an NRI, investing in a recurring deposit account is a smart move. Why? Because there are no major risks involved, you earn a consistent interest rate and cultivate a savings habit that eventually builds a good corpus in India.

NRI recurring deposit accounts offer attractive tax benefits, high interest rates, and peace of mind. Open Yours Today With Savetaxs.

The following table compares whether a recurring deposit is better for NRIs or a fixed deposit.

| Comparision Factor | RD Account For NRIs | FD For NRIs |

|---|---|---|

| Investment Method | Fixed amount deposited every month | One-time lump sum deposit. |

| Best suited for | NRIs with a regular monthly surplus. | NRIs with idle lump sum funds. |

| Minimum Investment | A low monthly commitment | A larger initial investment is needed. |

| Interest rate | Relatively lower or similar to FDs. | Generally, higher than a recurring deposit. |

| Risk Level | Offers low risk | Offers low risk |

| Returns | The returns are moderate and predictable. | The returns are higher and more predictable. |

| Flexibility | Quite limited once RD starts. | Offers much more flexible tenure options. |

| Premature Withdrawl | Allowed, but a penalty is imposed | Allowed, but a penalty is imposed. |

| Taxation (NRE) | Interest is tax-free in India. | Interest is tax-free in India. |

| Taxation ( NRO ) | Interest is taxable with TDS. | Interest is taxable with TDS. |

| Repatriation | Depends on NRE/NRO linkage. | Depends on NRE/NRO linkage. |

| Ideal Use Case | Makes you disciplined with respect to long-term savings. |

Parking surplus money safely in India. |

For an NRI, an NRI RD account is one of the safest and most secure savings options if you are seeking assured returns with no market risk. An RD encourages the investor to deposit a fixed amount each month, which cultivates a disciplined habit.

Additionally, before making any decision, you must understand that NRO and NRE RDs are different from each other, especially in terms of taxation, repatriation, exchange rate, documentation, and exposure.

However, as an NRI, if you are seeking professional assistance to help you analyze the right RD account as per your financial plan, an expert-approved savings plan, and a better understanding of which bank offers the best RD interest rates for NRIs, then Savetaxs is the name to trust.

We have been managing the RD accounts of NRIs from 60+ countries, confidently investing in India without any non-compliance and building a generous corpus.

Our experts will help you choose the right NRI RD that best suits your financial plan, taxation, and repatriation preference. Connect with us as we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr Shaw brings 8 years of experience in auditing and taxation. He has a deep understanding of disciplinary regulations and delivers comprehensive auditing services to businesses and individuals. From financial auditing to tax planning, risk assessment, and financial reporting. Mr Shaw's expertise is impeccable.

Want to read more? Explore Blogs

_1769758257.webp&w=828&q=75)