Dividend Stocks in India for NRIs

Read More

_1771937622771.webp&w=3840&q=75)

As an NRI, if you are planning to spend your golden years of life after retirement in India, then an NRI retirement plan is hands down the most suitable option for you. A retirement plan is a savings and investment instrument for NRIs that helps them accumulate funds for long-term financial security.

This strategic approache ensure you are financially well prepared to live a retired life free from financial strain. Furthermore, a good NRI retirement plan in India offers a range of benefits, including flexible fund repatriation, tax savings, and a consistent source of income.

In this guide to retirement plans for NRIs, we will discuss each aspect, including eligibility, features and benefits, how to purchase a suitable retirement plan, types of retirement plans, tax benefits for retirement plans, and more.

After years spent abroad, working across different time zones, a good retirement is what every NRI deserves. However, most countries have dedicated retirement plans, but these may not be sufficient to meet the specific requirements of NRIs.

Henceforth, an NRI needs a retirement financial plan that is tailored to their retirement goals, flexible, and considers key factors such as inflation estimates, risk tolerance, current cost of living, ongoing health care needs, family dependents, and emergencies.

Let us understand why NRIs require a dedicated retirement plan.

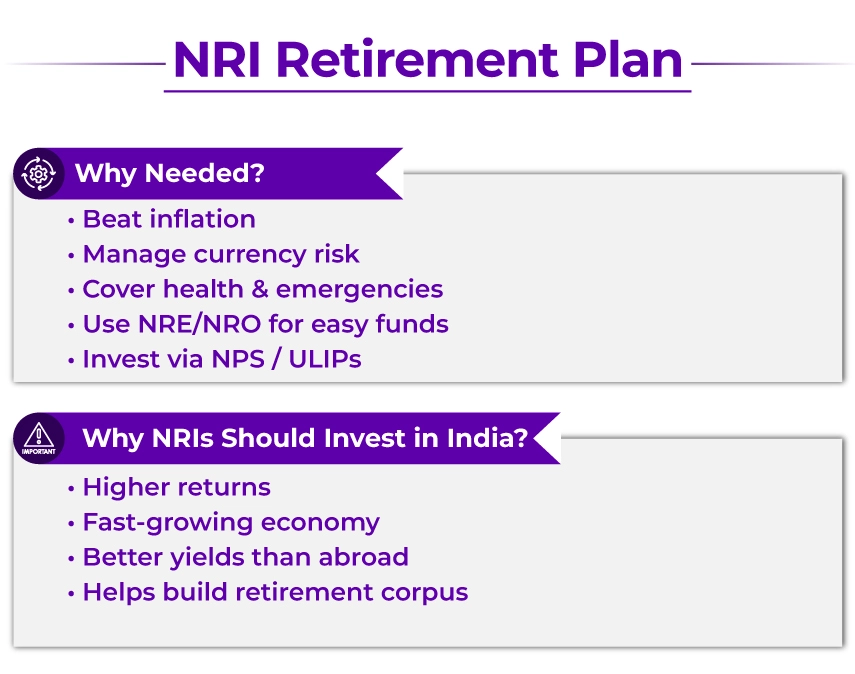

NRIs need a dedicated retirement plan to protect their finances from inflation. To do so, you can diversify your portfolio by investing in multiple retirement plans such as ULIPs, annuity plans, and the NPS.

To protect your income earned overseas from any exchange rate variation via a strategic repatriation strategy. Many NRI financial consultants suggest that NRIs planning their retirement retain a portion of their savings in either in dollor or euro-denominated currencies. A stable foreign currency can definitely hedge against future uncertainty.

The Non-Resident External (NRE) and Non-Resident Ordinary (NRO) accounts help NRIs manage their finances worldwide easily and smoothly.

The following are the types of retirement plans NRIs can choose from, depending on their future financial goals, risk tolerance, age, and other factors.

ULIP pension plan is a long-term insurance product that offers dual benefits of insurance and investment. The premium paid for such plans is divided, with one part covering life and the other invested in other market-linked activities.

NRIs can invest in multiple instruments, such as equity, debt, and a balanced fund, while receiving life insurance coverage. This way, NRIs can capitalise on both long-term wealth growth in India and life insurance coverage.

This type of plan is a contact between an annuitant and the insurer. These are the dividends in achieving the annuitant's financial goals, with guaranteed income during the retirement phase. By starting with small investments well before retirement, NRIs can build a substantial retirement corpus.

NRIs need an NRO account to invest in such annuity plans for NRIs. This plan not only allows the investor to save their own money but also gives them the flexibility to hold their funds on a quarterly, annual, or monthly basis.

NPS is a retirement scheme that enables NRIs to build a regular source of income or a retirement pension. In these schemes, NRIs can invest in NPS Tier 1 annually until maturity. On maturity, NRIs must use a portion of the National Pension Scheme (NPS) corpus to purchase an annuity; pension income depends on the annuity chosen and is not guaranteed by NPS itself.

Apart from the ones mentioned above, EPF may apply based on employment status, but APY and PMVVY are meant for resident Indians and are generally not available to NRIs.

APY and PMYY are slid government-backed pensions. APY is an excellent choice for those working in the organic sector and holding an Indian bank account, whereas PMYYY is suitable for senior citizens.

For NRIs investing in India, there are several advantages the country offers over other countries, such as high interest rates and a fast-growing economy.

Here are some reasons why NRIs should invest in India.

Better Interest Rates - India has been offering attractive returns across multiple investment plans, such as market-linked ULIPs and retirement plans, helping investors combat inflation.

A Rapidly Growing Economy- India is a leading economy, one of the fastest growing economies, fueled by a huge economic market and a young population, offering plenty of investment opportunities.

Higher Yields: India's equity and debt markets offer returns considerably higher than those of many other developed nations, despite lower interest rates.

The NRI retirement plans in India have two different phases:

The very first step is the contribution phase, during which the retirement plan is established, and NRIs begin participating in investing and savings.

The second phase is when the direct buttons are pushed, and investors start to enjoy their retirement investments.

The following are the features of the retirement plan for NRIs:

Contribution Flexibility: NRIs are often given the option to choose between a lump-sum and regular pre-tax contributions. Not only this, but NRIs also enjoy full freedom to choose policy terms. This flexibility allows NRIs to stay in sync with their earning patterns abroad.

Currency Options: Understanding NRI currency movements across borders is essential for financial planning. NRIs can choose to invest in INR or in any other stable currency, such as the US dollar or the Euro. Doing so will help NRIs manage long-term forex risks. Financial experts suggest that advanced investors invest in currency futures or options, which, in the long run, help them manage currency volatility.

Multiple Payout Modes: It depends on the type of pension plan and your future goals for how you choose to get retirement income. Some of the best retirement plans offer flexibility, allowing investors to choose the optimal payout method.

For instance, if an investor chooses a monthly payout from their deferred annuity plan, they can expect a fixed, consistent monthly income for a predetermined period. If they choose a lump-sum payout, then they will receive a major portion of their insurance coverage in one go, and can see it as per their preference.

Investment-Linked & Guaranteed Options: The return depends on the type of retirement plan you have chosen. For instance, if you choose ULIPs that offer a market-linked investment feature and life insurance coverage, the return will depend on how their underlying funds perform in the market.

Whereas investing in an annuity plan will assure guaranteed income, as this plan is a type of non-linked financial instrument.

Global Accessibility: Being globally accessible is indeed one of the best features of retirement plans for NRI. Regardless of which country you are residing in, NRIs can easily access their retirement funds and can customize their investment portfolios seamlessly.

Whether you continue investing in your retirement plans or withdraw your funds, the entire process will be seamless.

The following are the factors NRIs must consider before locking in their investments in retirement plans in India.

NRIs must know that the investment value of their NRI retirement plan depends not only on how their plans perform, but also on currency fluctuations. If the NRI's resident currency depreciates against the Indian currency, the retirement plan's return might be reduced when repatriating the funds.

Repartition of funds is a tricky concept in some of the retirement investment plans; you have to put in extra effort to determine whether the retirement plan you choose falls under the easy repartition category or not. And if it is easy, then what rules of repartition should you follow? For instance, under the Foreign Exchange Management Act, NRIs should repatriate up to USD 1 million of the principal amount of their NRO account. Whereas the account's interest amount is repatriated separately.

Picking the right lock-in period ensures your funds grow uninterrupted and that you develop a disciplined savings habit. NRIs: Before investing in a retirement plan, please ensure the risk is aligned with your regular income.

When, as an investor, you are well aware of your risk appetite, it helps you choose the best retirement plan for NRIs. As an NRI investor, some prefer a balance between a safe income and high growth opportunities, whereas some of the investors like to play with risk and aim higher, and hence choosing a plan that fits well with your risk appetite is necessary. It is advisable to conduct prior research and compare different plans before you invest in one.

When making any investment as an NRI, it is important that NRIs are familiar with the regulations of IRDAI, FEMA, RBI, and SEBI. Furthermore, to comply, NRIs must also maintain proper documentation, including updated KYC, bank statements, address, and identity proof.

For NRIs to have a happy retirement life after hustling all through their lives, there is no better alternative than a retirement plan. The following are the primary NRI retirement plans benefits.

Indian retirement plans offer NRIs a stable, regulated framework compared to those in other countries, helping you secure your financial future. Be it attractive returns from a diversified portfolio with minimal risk or a consistent lifetime income stream, NRI retirement plans are a beneficial choice.

NRIs planning to spend their retirement lives in India should prioritize building a robust retirement corpus to avoid financial struggles. Inevitably, diversification of long-term retirement corpus in India creates wealth over time.

Plans such as life insurance plans and deferred annuities offer NRIs a steady income source post-retirement. This makes it easier for NRIs to manage their lifestyle, daily expenses, utility bills, and medical emergencies, ensuring their golden years are peaceful and stress-free.

The following is the eligibility criteria for NRIs to invest in an NRI retirement plan.

For NRIs to apply for an NRI retirement plan, follow the steps given below.

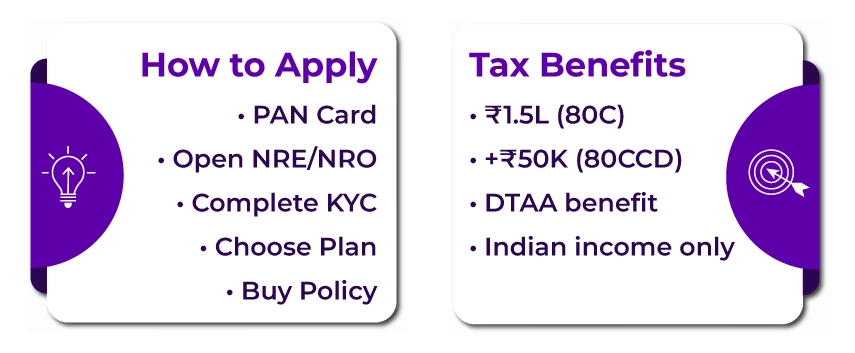

Step 1: Get a PAN Card: For NRIs, a PAN card is mandatory for any investment or financial transactions in India, and it's needed ot get you an NRI retirement plan too.

Step 2: Open an NRO or NRE bank account: If you do not already have an NRI-designated account, you must open one to invest in an NRI retirement plan in India. For this, reach out to any legitimate Indian bank and open an NRO and NRE bank account for financial transactions in India.

Step 3: Complete KYC and Other Documentation: NRIs must comply with the Know Your Customer (KYC) requirements, as this is non-negotiable. Provide your insurer with all required documents, including a passport, visa, or residence permit, and complete the verification process.

Step 4: Choose the Insurer & Retirement Plan: Select a reliable insurer and a suitable retirement plan that aligns with your long-term financial goals.

Step 5: Complete the proposal form and purchase: After selecting the desired retirement plan, obtain the application form from the insurer and complete it. Provide all the details needed to facilitate the purchase.

NRIs must ensure that, when applying for a retirement plan, they consider both Indian and the tax laws of their country of residence, and adhere to all applicable regulations.

The following are the tax benefits for NRIs that they can enjoy with retirement plans in India, as per the following provisions of the Income Tax Act.

The following are the steps that NRIs can follow to buy an NRI retirement plan in India.

Step 1: First and foremost, get and compare available plans from different insurers in India. Now, before you apply for the retirement plan in India, go through the terms and conditions of each policy, along with the benefits, and how well each policy aligns with your long-term goals. Once all the checks are done, choose asuitable plan for you.

Step 2: Once the suitable retirement plan is selected, get the proposal from the insurance company. accurately fill out all required information for your insurance plan, including your name, address, gender, date of birth, phone number, email address, and so on.

Step 3: Then state how you would like to pay the premiums, that is, regular payments in a lump-sum way.

Step 4: The insurer will then provide you with all the information on the qualified remittance plans based on your selection.

Step 5: Next, choose the payout option that suits you best.

Step 6: After selecting the relevant NRI, determine the required premium amount. You can furthermore check the premium by using an online calculator.

Step 7: Now upload all required documents, such as a residential permit, visa, passport, and NRE or NRO bank details, as requested by your insurer. Please ensure you adhere to all Indian regulations for the NRI investment process.

Step 8: Lastly, make the due payments and activate your pension plan.

Once the payment is completed, you will receive the purchase details and the policy documentation. You can also monitor your retirement plan regularly and then reach out to the insurer whenever you want to make any changes in the policy to suit your changing needs.

We help NRIs file their NRI ITR in India seamlessly.

Retirement plans for NRIs offer stability during their golden years. But yes, for NRIs, finding a trusted and reliable retirement plan can be overwhelming. To find one, an NRI can definitely seek advice from NRI investment advisers and professionals to find the right plan that fits their personal and financial goals.

NRIs, even a small mistake can be an expensive affair; hence, research well before you lock in your hard-earned money in any retirement investment plan.

However, as an NRI, if you are seeking professional assistance in selecting the right NRI-centric retirement plan that offers attractive and stable returns with minimal risk, Savetaxs is the name to trust. Our experts will help you manage complex cross-border finances and ensure 100% regulatory compliance with FEMA, RBI, and SEBI.

Connect with us as we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr. Ritesh has 20 years of experience in taxation, accounting, business planning, organizational structuring, international trade financing, acquisitions, legal and secretarial services, MIS development, and a host of other areas. Mr Jain is a powerhouse of all things taxation.

Want to read more? Explore Blogs