NEFT, RTGS, IMPS Fund Transfer : Which is better for NRIs?

Read More

_1771333101892.webp&w=3840&q=75)

Many NRIs use Indian bank accounts to manage their income earned in India or their resident country, invest in Indian assets, repatriate funds, or meet financial needs. If these accounts are not used for a specific period, the bank will mark them as dormant or inactive. Given this, activating dormant accounts for NRIs is vital for maintaining financial ties with India. Additionally, it ensures ongoing access to investments and funds.

Further, having an active NRI bank account ensures uninterrupted financial control, smooth access, and fewer compliance steps. Confused, how to keep your bank account active in India? In this blog, you will learn everything about an NRI dormant bank account, why it becomes inactive, and how to reactivate it with ease. So read on and clear all your doubts.

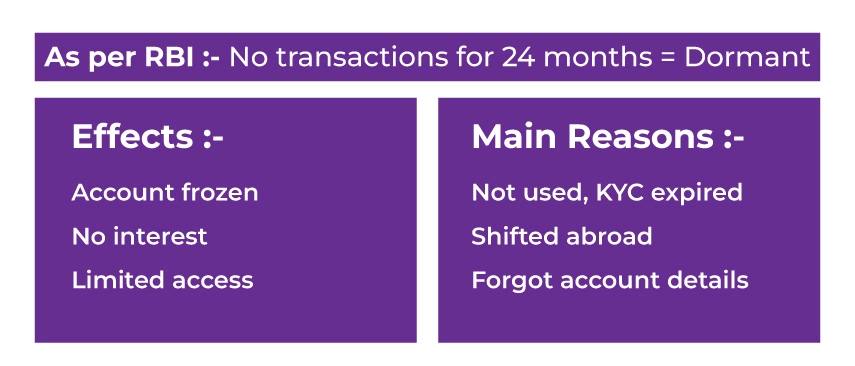

According to the Reserve Bank of India (RBI), if you do not use your NRI bank account for any transactions in the last 24 months, then it is classified as dormat account. Here, the transactions include activities like fund transferring, cash withdrawal, payment made with cheques, and more. Further, service charges or interest credits are not included in transactions.

The following are the key characteristics of an NRI dormant bank account:

Additionally, a dormant account can lead to several inconveniences. It includes accumulated interest, or is not able to access funds. Hence, if your NRI account becomes dormant, it is vital to reactivate it.

This was all about a dormant NRI bank account. Moving ahead, let's know the difference between an inactive account and a dormant account.

The table below provides a detailed comparison between an inactive bank account and a dormant bank account, offering clarity to NRI account holders.

| Aspects | Inactive NRI Bank Account | Dormant NRI Bank Account |

| Duration of inactivity | If you do not use your NRE/ NRO bank account to transact for more than 12 months, it is classified as inactive. | If there are no transactions made for a continuous two years, it is marked as a dormant account. |

| Criteria for inactivity | There are no restrictions imposed on an inactive NRI bank account. Considering this, it allows both credit and debit transactions. You can take non-financial actions like checking your balance or logging in. | If the account is stated as dormant, all your financial actions are restricted. Although you can log in via mobile banking or net banking but cannot conduct any financial activities. |

| Reactivation process | To reactivate your inactive account, you generally need to do a transaction. For instance, making a withdrawal, deposit, or connecting with your bank to express your intention to continue using it. | In the dormant account, the reactivation process is more complex. For instance, to reactivate your dormant NRI account, you need to fill out the application along with your KYC information. |

| Interest accrual and fees | In the inactive account, interest continues to accrue as per the terms and conditions of the account. However, from the balance amount, maintenance or other service fee still be deducted. | IInterest continues to be credited even in dormant accounts, and banks are not allowed to levy penal charges solely due to dormancy., specific to dormant accounts, or take reactivation fees when you want to access your funds again. |

| Unclaimed funds | Funds are not transferred or treated as unclaimed. In the inactive account, the key focus remains on administrative or maintenance charges. | If, for a longer period, the dormant account remains inactive, banks may transfer the balance amount to the Depositor Education and Awareness Fund (DEAF) managed by the RBI. |

So, here is how a dormant NRI account is different from an inactive account. Moving further, let's know when the NRI account becomes dormant.

An NRI bank account becomes dormant because of the following reasons:

When NRIs unexpectedly move to a new place, primarily because of a job, not changing the bank details is a common thing. During relocation, it is vital to change your contact details. It results in better communication between you and your bank.

Bank accounts maintained in India generally need to be more active. Often, because of this, small accounts get ignored when, to some extent, they are concerned with proper upkeep. Additionally, NRIs, for several reasons such as investments, savings, or meeting family expenditures, have multiple bank accounts. Considering this, with time, accounts open for single transactions or small balances get dormant.

Setting up their financial transactions overseas and access to better banking NRE & NRO accounts in India are likely to be less used by NRIs. This specifically happens when a more appropriate and immediate online services offered by foreign banks fit the banking activities of NRIs.

The most common technical cause of dormancy is the expiry of KYC documents. At creating times, documents like ID proof, address proof, and visa are updated by the bank. Often, NRIs residing overseas find it difficult to provide these documents. Considering this, failure to meet the submission deadlines or difficulties in submitting updated documents result in dormancy.

Another key issue is forgotten or misplaced account codes or IDs. When moving from one country to another, losing cash, banking documents, debit cards, or chequebooks is a common issue. Additionally, long-term system inactivity causes forgotten identification details and passwords. It further creates more complex issues that increase the security of an account.

These are some of the key reasons why an NRI account becomes dormant. Moving ahead, let's know the RBI rules on dormant accounts for NRIs.

The regulations and policies of NRI account activation are aligned with the Reserve Bank of India (RBI). These regulations are stated under FEMA and are supported by certain circulars relating to the banking mechanism of NRI. Considering this, the basic principles of RBI involve several essential aspects of managing inactive accounts:

These were some of the RBI rules on dormant accounts for NRIs. Moving further, let's know about what happens when an NRI account becomes dormant.

If your NRI account becomes dormant, you will not be able to avail of services like internet banking, cheques, request for debit cards, and other banking transactions. Apart from this, services like phone banking and ATM transactions also become unavailable.

So this is what happens when an NRI account becomes dormant. Moving ahead, let's know how to reactivate a dormant NRI account.

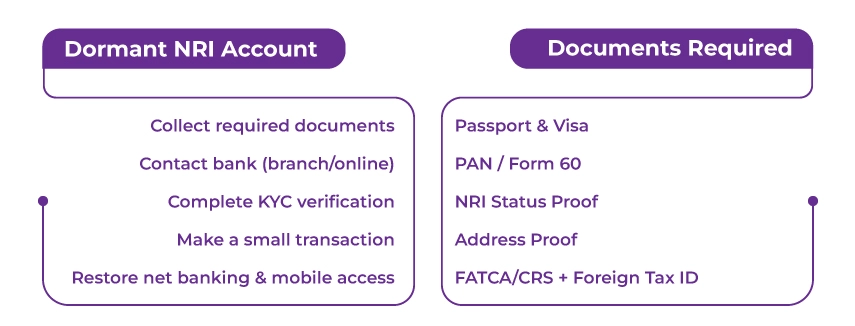

NRIs to reactivate a dormant account need to follow the steps below:

Step 1: Document Preparation

Step 2: Bank Communication

Step 3: Verification Process

Step 4: KYC Updation

Step 5: Account Reactivation

Step 6: Access Restoration

This is how, using the above steps, you can reactivate your NRI dormant account. Moving further, let's know about the documents required to reactivate your dormant account.

To reactivate your dormant NRI bank account, you need to following documents:

These were the documents you needed to submit during your dormant account activation. Moving ahead, let's know if NRIs from abroad can activate their dormant account.

Yes, NRIs can activate a dormant account from abroad. For this, they need to submit a written reactivation request, updated KYC documents, and do a bank transaction. Additionally, the account activation process can be completed online banking, via email, courier, or video KYC.

So, from the above information, it is clear that yes, NRIs can activate a dormant account from abroad. Moving further, let's know the minimum transaction required to activate the account.

There is no minimum transaction limit to activate the dormant account. However, generally, a token amount is stated to ensure the transaction is recognized. Considering this, valid transactions include deposits, transfers, bill payments, or ATM withdrawals. Additionally, automatic transactions like interest credits are not counted in activation.

This was all about the minimum transaction requirement to activate the NRI account. Moving ahead, let's know how to avoid your NRI account becoming dormant.

To avoid your NRI account becoming dormant, ensure you do one customer-initiated transaction. It includes withdrawal, deposit, or transfer made every 12 to 24 months. Additionally, monitor your account regularly via net banking, and set up automatic transfers. Also, keep your documents updated for KYC to prevent your NRI account from becoming inactive.

This is how you can avoid your NRI account becoming dormant.

Connect with Savetaxs, simply open an NRI savings account in India and get preferential rates on your remittances.

Lastly, having an active NRI account is helpful when you conduct financial transactions and investments in India. Additionally, the process of reactivating dormant accounts for NRI is a simple process. For this, they need to contact their bank, provide updated information, fill out necessary forms, and make a transaction.

Further, if you need NRI banking assistance, connect with

We have a team of financial experts who assist you in resolving all your banking queries and managing your accounts in India.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr. Ritesh has 20 years of experience in taxation, accounting, business planning, organizational structuring, international trade financing, acquisitions, legal and secretarial services, MIS development, and a host of other areas. Mr Jain is a powerhouse of all things taxation.

Want to read more? Explore Blogs