_1770814049668.webp&w=828&q=75)

How NRIs Close SBI Accounts Online and Offline?

Read More

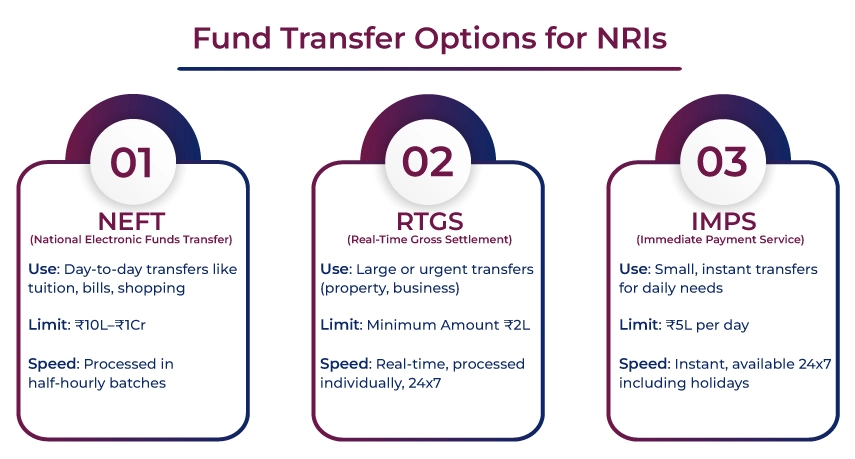

An NRI can use NEFT, RTGS, or IMPS to transfer funds between bank accounts in India, depending on the urgency and amount of the transaction. The difference between these three methods mainly lies in their transfer limits, settlement speed, and purpose of use.

IMPS allows you to transfer money 24×7, including bank holidays, and is operated by the NPCI (National Payments Corporation of India). Most banks allow transfers from ₹1 up to ₹5 lakh per transaction, though limits may vary depending on the bank.

On the other hand, NEFT and RTGS are bank transfer systems managed by the Reserve Bank of India (RBI).

In this blog, we will discuss these three transfer methods and understand the difference between NEFT, RTGS, and IMPS, including their processing times, limits, and costs, to help NRIs make a smarter decision when transferring funds in India.

NEFT, RTGS, and IMPS are three electronic fund transfer systems that allow NRIs to transfer funds between bank accounts in India.

These transfer methods differ in processing speed, transaction limits, and purpose.

NEFT (National Electronic Funds Transfer) processes transactions in half-hourly batches throughout the day. Since NEFT does not have a minimum transfer limit, it is commonly used for regular payments such as tuition fees, bill payments, or small transfers.

Banks may impose transaction limits such as ₹10 lakh or ₹1 crore per transaction through internet banking, depending on the customer segment.

RTGS (Real-Time Gross Settlement) is designed for large-value transactions with a minimum transfer amount of ₹2 lakh. RTGS processes transactions individually in real time, meaning the funds are credited to the beneficiary account almost immediately.

RTGS is commonly used for high-value transactions such as property purchases, business investments, or large transfers.

The third method is IMPS (Immediate Payment Service), which is commonly used for small and urgent transactions.

IMPS allows users to transfer money instantly, 24×7, including bank holidays. The typical transfer limit is up to ₹5 lakh per transaction, although it may vary depending on the bank.

IMPS is generally used for quick transfers, family support, or daily financial needs.

Although UPI has expanded internationally in some countries like Singapore and the UAE, it is mainly used for merchant payments and domestic transfers, and it is not typically used for large remittances or repatriation transactions.

If an NRI wants to transfer funds from an NRO account to an NRE account or repatriate funds abroad, proper documentation is required to comply with FEMA regulations.

The bank may request the following documents:

Additionally, the following compliance documents are usually required:

As per FEMA regulations, NRIs are allowed to repatriate up to USD 1 million per financial year from their NRO account, provided all applicable taxes have been paid.

After verifying the tax liability, a Chartered Accountant issues Form 15CB, which confirms that the applicable taxes have been paid before transferring the funds.

Each transfer method has different limits and processing speeds, which affect how NRIs choose to transfer funds.

Transaction Limits

NEFT processes transactions in half-hourly batches, which means the transfer may take 30 minutes to a few hours depending on the batch cycle.

RTGS transactions are processed individually and in real time, meaning the beneficiary account is usually credited immediately.

IMPS provides instant settlement and works 24×7 throughout the year, making it suitable for urgent transfers.

| Feature | NEFT | RTGS | IMPS |

| Availability | 24×7×365 | 24×7×365 | 24×7×365 |

| Settlement Type | Batch Processing | Real-Time Settlement | Instant |

| Processing Speed | 30 minutes – few hours | Immediate | Instant |

| Minimum Amount | ₹1 | ₹2 lakh | ₹1 |

| Maximum Amount | No RBI limit | No upper limit | Up to ₹5 lakh (bank dependent) |

Banks are generally required to credit RTGS transactions within 30 minutes after receiving the funds.

NRI transfers may involve different direct and indirect costs, which can affect the final amount received.

In some cases, the exchange rate margins and intermediary bank charges may increase the overall cost of transferring funds. These charges may vary depending on the bank and the transfer method used.

For online NEFT and RTGS transactions, most banks do not charge any transfer fee.

IMPS charges may vary depending on the bank and transfer amount.

Typical IMPS charges are:

| Transaction Amount | Charges |

| ₹1 – ₹1,000 | ₹3.50 + GST |

| ₹1,001 – ₹1,00,000 | ₹5 + GST |

| Above ₹1,00,000 | ₹15 + GST |

When determining the best transfer method, consider various factors that affect your remittance success.

When choosing the best transfer method, NRIs should consider several factors.

Exchange rates can significantly affect the final transfer value. Monitoring exchange rate trends may help you secure a better deal.

The amount being transferred also determines the best method:

Banks use several security measures to protect transactions, including:

NRIs should avoid using unsecured networks when accessing their bank accounts and regularly monitor transaction activity.

Understanding the differences between NEFT, RTGS, and IMPS helps NRIs choose the most suitable method when transferring money in India.

IMPS is ideal for urgent transfers up to ₹5 lakh, as it operates 24×7.

RTGS is designed for high-value transactions above ₹2 lakh, such as property purchases or large investments.

NEFT works well for routine transfers of any amount and is widely used for everyday banking transactions.

The best option depends on the transfer amount, urgency, and purpose of the transaction.

If you need assistance choosing the right transfer method or understanding NRI banking rules, the experts at SaveTaxs can help guide you through the process.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr Manish is a financial professional with over 10 years of experience in strategic financial planning, performance analysis, and compliance across different sectors, including Agriculture, Pharma, Manufacturing, & Oil and Gas. Mr Prajapati has a knack for managing financial accounts, driving business growth by optimizing cost efficiency and regulatory compliance. Additionally, he has expertise in developing financial models, preparing detailed cash flow statements, and closing the balance sheets.

Want to read more? Explore Blogs

_1771580892112.webp&w=828&q=75)

_1771333101892.webp&w=828&q=75)

Yes, NRIs can use NEFT, RTGS, or IMPS through their NRE or NRO accounts to transfer funds to accounts in India. However, it depends on where they are transferring. If they are transferring to a local resident account, then no documentation is required. If transferring to an NRE Account, then it is subject to compliance with banking and foreign exchange (FEMA) rules.

The transfer limits for each method are as follows:

IMPS method is fully available 24*7, including holidays. On the contrary, NEFT and RTGS have expanded their availability, with many banks supporting round-the-clock services.

RTGS is usually preferred for high-value transfers (above Rs. 2 lakhs) as it provides immediate real-time settlement without batching delays.

IMPS fees may differ depending on the transfer amount, while online NEFT and RTGS transfers usually have zero charges.