_1770447889455.webp&w=828&q=75)

What are the Punjab National Bank SWIFT Codes?

Read More

When investing in Indian shares and other securities, when you open a demat account, you may see a document, i.e., Power of Attorney (POA). Often, during the demat account opening process, this document is presented by your Depository Participant (DP) or stockbroker. It plays a vital role in managing and executing transaction tasks effectively in your demat account.

Confused? This blog provides you with complete information on POA in a demat account. It further helps you in understanding what a power of attorney actually is, why brokers may request it for operational convenience., and more. So read on and clear all your doubts about it.

Power of Attorney, or POA, is a legal document through which you (the investor) give specific powers to another individual or entity (generally your stockbroker or DP) to perform certain activities on your behalf. It includes activities like selling shares, debiting the demat account, transferring securities, and settling trades.

In the context of a demat account, an individual with POA can execute trades and handle transactions related to securities without needing the signature of the investor each time. Additionally, a POA holder represents you in situations where you can't appear physically.

Further, it is not mandatory to have a PoA to open a demat account; it is optional. However, for NRIs, hiring a PoA in a demat account is a beneficial option. It certifies smooth functioning specifically for online trading. Also, in the absence of PoA, you need to authorizes you transaction manually. It may result in delayed order execution and missed opportunities.

Now, let's know the activities covered under POA:

Moreover, by granting POA, you allow an individual to handle the above-mentioned activities without needing your separate delivery instructions for each transaction. However, it is vital to understand the extent of the authority you are providing and ensure it matches your trading habits.

This was all about POA in a demat account. Moving ahead, let's know the POA in the demat account for NRIs.

Connect with Savetaxs and get assistance with your NRI taxation from financial experts, and maximize your returns.

Since NRIs are not always physically present in India to approve each transaction, a POA is although optional for NRI demat accounts. However, it plays a vital role. In the absence of it, NRIs might need to spend extra time in India to sign paperwork whenever they need to purchase or sell shares.

Similarly, it also delays the execution, which might result in missing opportunities in a stock marketplace that moves quickly. However, with a POA, authorized brokers or depository participants can conduct transactions on behalf of NRIs easily on permitted transactions. It certifies adherence to purchasing, selling, and settling legal guidelines and reducing operational inefficiencies.

This was all about the role of POA in an NRI Demat account. Moving further, let's know the key difference between a POA vs e-DIS/ CDSL TPIN.

The table below showcases the key differences between POA and e-DIS/ CDSL TPIN:

| Feature | POA (Power of Attorney) | e-DIS/ CDSL TPIN |

|---|---|---|

| Meaning | It is a legal document that authorizes the broker to execute the transactions strictly as per the instructions of investors without any discretionary investment decision-making. | It is a digital authorisation given by the investor using TPIN (transaction personal identification number), a six-digit numeric password, authorizing share debits from the CDSL demat accounts. |

| Permission Type | One-time authorisation with continuous permission. | For each sale transaction, permission is required. |

| Control | Control depends on the scope of the POA granted; SEBI mandates limited-purpose POAs. | Investors have full control. |

| Share Debit Process | For settlement, the broker can automatically debit shares. | Once the TPIN + OTP is approved, you can debit shares only then. |

| Security Level | Medium, but it depends on the trust of the broker. | High as every time you get OTP-based approval. |

| Convenience | High, as there is no requirement for OTP each time. | Moderate, as for authorisation, OTP is required. |

| Misuse Risk | Possible if the POA is misused or broad. | Misuse risk is very low as OTP is required. |

| Best For | Frequent traders | Long-term investors, NRIs, and safety-focused users |

| Cancellation | Requires POA revocation process. | TPIN can be disabled/ reset easily. |

| Requirement Today | Optional | By default, it is commonly used by most brokers. |

Further, eDIS (electronic delivery instruction slip) in 2020 was replaced by the CDSL TPIN. Although in a few scenarios, eDIS is still used, CDSL TPIN is the primary mechanism now used by brokers. It, without a POA submission, allows the sale of shares.

So, this was all about the key difference between POA and e-DIS/ CDSL TPIN. Moving ahead, let's know the key risks and regulatory safeguards around POA.

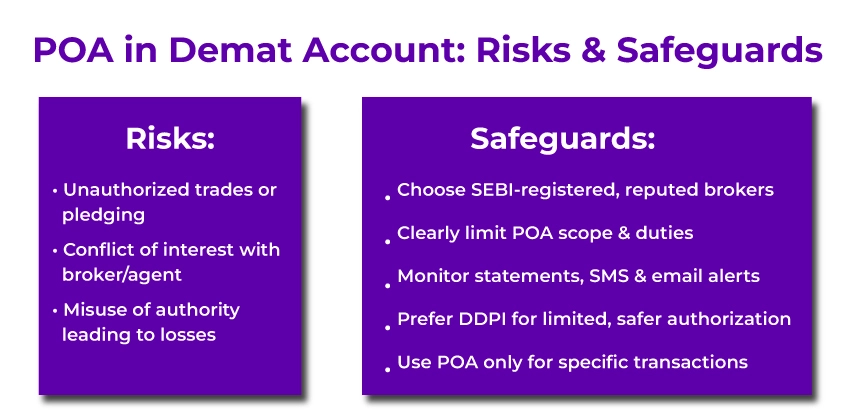

Here are some of the risks associated with POA in a demat account:

Further, here are some of the safeguards that you should consider. These are as follows:

These were some of the risks and regulatory safeguards around POA that an investor should consider. Now, moving further, let's know how to revoke or modify a POA in a demat account.

To revoke or modify your POA in a demat account, here is what you need to do:

Further, for some reasons, if you need to modify the POA, it is only possible by opening a new POA that overrides the existing one. Additionally, the changes/ modifications should be mentioned in it clearly so that you want to implement.

Get financial insights and advice from experts for informed investment decisions.

Lastly, a POA in a demat account is a tool of convenience for investors like NRIs, not a necessity. It is useful to manage your financial and non-financial transactions where you need to be present physically everywhere. Additionally, for specific or general purposes, you may transfer your authority to represent yourself to one or more persons.

Further, if you need any assistance and guidance with NRI investments, connect with Savetaxs. We have a team of financial experts who can help you resolve your financial doubts and choose the best investment as per your goals and risk tolerance.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr. Ritesh has 20 years of experience in taxation, accounting, business planning, organizational structuring, international trade financing, acquisitions, legal and secretarial services, MIS development, and a host of other areas. Mr Jain is a powerhouse of all things taxation.

Want to read more? Explore Blogs

-Bank-Account_1770727847365.webp&w=828&q=75)

_1770709078772.webp&w=828&q=75)

_1770800720708.webp&w=828&q=75)

_1770814049668.webp&w=828&q=75)