The ITR-3 (Income Tax Returns) is designed for individuals, NRIs, and Hindu Undivided Families (HUFs) with income from the head, receiving profits or gains from business and profession, and who are required to maintain comprehensive books of account. Additionally, individuals earning income from salaried employment and other sources, such as freelancing or part-time business activities, can use the ITR-3 to file their income tax returns until they have business income.

The Income Tax Department of India (IT) has prescribed ITR-3 for different types of taxpayers. This guide will walk you through the significance of the ITR-3 form. We will discuss what ITR-3 is, who can and cannot file it, and how an NRI can file it.

- ITR-3 is an income tax return form used by NRIs and HUFs receiving income from specific sources.

- The deadline for filing ITR-3 has been extended from 31st July 2025 to 15th September 2025 for accounts that don't require an audit.

- The due date for accounts that need an audit is the 31st of October.

- The ITR-3 form has now been updated to include Section 44BBC, simplifying compliance.

What Is the ITR-3 Form for NRIs? (Meaning & Purpose)

ITR-3 is an Income Tax Return form used in India for individuals, NRIs, and Hindu Undivided Families (HUFs) who have income from the following sources:

- Income from capital gains

- Income from salary or pension

- Income from house property

- Income from business or profession

- Income from other sources

You can also call it a master form because it is the one form in which an individual or HUF can report all their possible incomes. However, the taxpayer must have a proprietorship or a business as one of their sources of income to be eligible to file the ITR-3.

The ITR-3 is a more thorough form, allowing the taxpayer to add more detailed information about their income and deductions across different sources. The form has several sections where the individual needs to fill in relevant information, such as personal details, taxes paid, deductions, income from various sources, verification, and the calculation of total income.

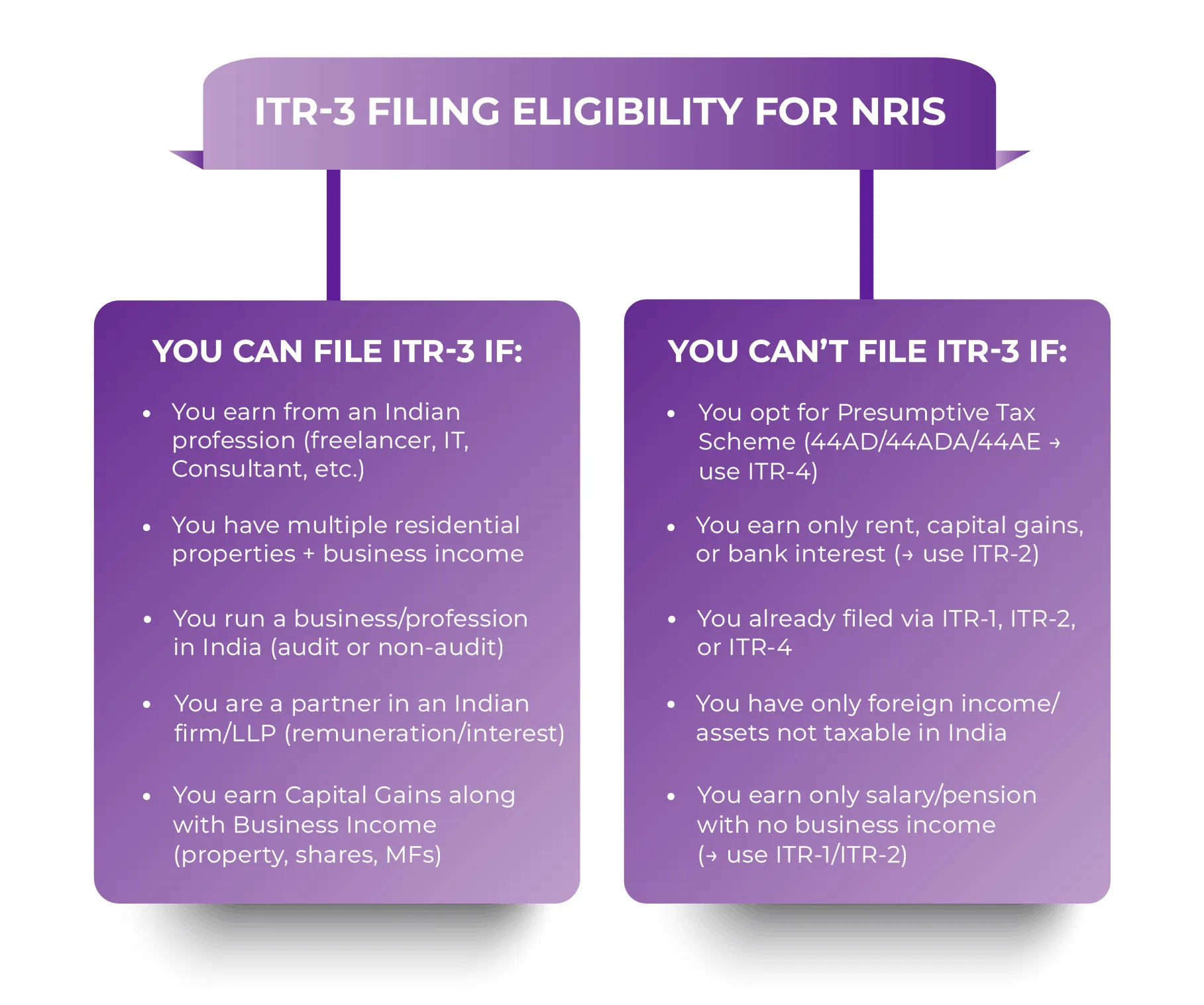

Who Is Eligible to File ITR-3 as an NRI?

Not everyone can file ITR-3. Individuals who fall in the following categories will be eligible to file ITR-3 as an NRI:

- NRIs who receive income from an Indian profession, such as freelancing, consulting, IT, advisory, design, or content.

- An NRI who holds multiple Indian residential properties along with business income.

- Individuals who are carrying on a business or a profession in India, regardless of whether it is a tax audit or a non-audit case.

- An NRI who is a partner in an Indian partnership firm/LLP and receives interest or remuneration from the firm.

- NRIs who are earning Capital Gains on an Indian asset, along with business income, can include a house property, shares, or mutual funds.

Who Is Not Eligible to File ITR-3?

- NRIs whose only income is from foreign assets or foreign income that is not taxable in India are not eligible to file ITR-3.

- ITR-3 is strictly for individuals, HUFs, NRIs, partnership firms, companies, LLPs, etc. Any other form of organisation must not file ITR-3 as they have different forms for filing their tax, such as ITR-5 or ITR-6.

- An NRI, individual, or HUF who is not receiving any income through the means of business, profession, or partnership firm cannot file the ITR-3 form. Like only rental, capital gains, bank interest, etc.

- A taxpayer who has already filed their tax return under ITR-1, ITR-2, or ITR-4 cannot file under ITR-3.

- An individual, HUF, or NRI who is not receiving any income from a business or profession must use ITR-2, regardless of whether they have rental income or capital gains.

- An individual who is choosing the presumptive taxation scheme under Section 44AD, 44ADA, or 44AE must not file ITR-3; instead, they should file ITR-4.

- A person whose income is from salaries or pensions and who has no business or professional income must not file an ITR using ITR-3. They should use ITR-1 or ITR-2.

ITR-3 Due Date for NRIs (AY 2025-26)

The due date to file ITR-3 for the financial year (FY) 2024-2025 (AY 2025-2026) has been extended from 31st July 2025 to 15th September 2025 for non-audit cases. The due date for accounts that require an audit is 31st October.

Latest Changes in ITR-3 Form for AY 2025-26

The following are some of the major changes in the ITR-3 form that have been made for the assessment year 2025-2026:

Section 44BBC Introduced: Presumptive Taxation for Cruise Ship Business

- The ITR-3 form now includes Section 44BBC, a newly introduced presumptive taxation provision under Budget 2024 that applies to non-resident cruise business operators. This section considers 20% of gross receipts from passenger carriage as taxable income for non-resident cruise operators.

- Adding this reference to the ITR-3 form simplified compliance by clarifying the reporting obligations for businesses operating in the cruise sector, ensuring they understand the specific tax rules that apply to their operations, and helping them follow them more effectively under the new taxation structure.

Capital Loss Treatment on Share Buybacks After 1 October 2024

- According to the new provisions, from 1st October 2024, capital losses incurred on share buybacks will be allowed if the corresponding dividend income is reported under the "Income from Other Sources" section.

- Taxpayers must ensure that dividend income is reported correctly to claim such losses under capital gains.

- This clarification adds transparency to the treatment of buyback-related transactions.

Capital Gains Split: Transactions Before and After 23 July 2024

- Capital gains will now be split under the amendments introduced by the Finance Act 2024; they must be split based on whether they arise before or after July 23rd, 2024.

- Taxpayers now need to categorise their capital gains accordingly and calculate taxes under the applicable provisions.

- This change aims to simplify the reporting of capital gains by clarifying the timeframes affected by amendments to the Finance Act, leading to a more straightforward tax treatment and compliance with the updated tax laws.

How Can an NRI File ITR-3 Online?

An individual, NRI, or HUF can file ITR-3 online by following the steps mentioned below:

Step 1: Log in to the Income Tax e-Filing Portal

Log in to the Income Tax India e-filing portal using your PAN number and password.

Step 2: Navigate to the ITR Filing Section

Go to the e-file menu and click on Income Tax Return> File Income Tax Return.

Step 3: Select the Correct Assessment Year

Select the period for which you are filing the return. Such as AY (Assessment Year) 2025-2026 for FY (Financial Year) 2024-2025.

Step 4: Fill in Income Details and Upload Required Documents

Select the form ITR-3 and fill out all the required details one by one, starting from personal details, then income, and then deductions. Once you have filled in the details correctly, upload the required supporting documents.

Step 5: Verify and Submit ITR-3

Cross-verify all the information you have entered and ensure everything is accurate and error-free. After that, submit the form. Verify using any of the following options: Aadhaar, OTP, EVC, or DSC, as it is a vital requirement.

Documents Required for Filing ITR-3 for NRIs

To file your ITR-3 (Income tax returns), you need the following documents:

- Indian Bank Account Details: Preferably, NRE/NRO account details are required. To provide refunds and the availability of financial details.

- Passport: To validate the residential status of an NRI, if required.

- PAN Card: It is important to identify the taxpayer and to file taxes in India.

- Books of Accounts: For an NRI who receives income from an Indian business or profession.

- Investment Details: To claim the deductions, including mutual funds, stocks, or property income in India.

- Foreign Assets/Income Details: Required if disclosure is required under the Indian tax laws, and if you were a resident in any financial year.

- Form 16 (if applicable): Received from the employer if you have income from Indian employment or contracts.

- Aadhaar (if applicable): An NRI doesn't necessarily need an Aadhaar card, but if they have one, they must link it to their PAN.

Get trusted guidance for NRI tax filing, planning, and cross-border strategies with ease.

Structure of the ITR-3 Form (AY 2024-25 vs AY 2025-26)

The ITR-3 comprises the following parts and schedules:

Part A

- Part A-GEN: General details and nature of the business.

- Part A-BS: Balance Sheet as of 31st March, 2021, for the proprietary business or profession.

- Part A-P&L: Profit and Loss: Profit and loss for the financial year 2020-2021.

- Part Trading Account: Trading account for the financial year 2020-2021.

- Part A-Manufacturing Account: Manufacturing account for the financial year 2020-2021.

- Part A-QD: Quantitative Details: It is optional if not subject to audit under Section 44AB.

- Part A-OI: Other Information: It is also optional if not subject to audit under Section 44Ab.

Schedules

- Schedule BP: Calculation of income from business or profession.

- Schedule S: Computation of income from salaries.

- Schedule AL: Assets and liabilities at the end of the year (applicable if the total income exceeds Rs. 50 lakhs).

- Schedule SI: Income statement, which is chargeable to tax at special rates.

- Schedule PTI: Details of pass-through income from either a business trust or investment funds according to Section 115UA, 115UB.

- Schedule FA: Statement of foreign assets and income from sources outside India.

- Schedule HP: Calculation of income under the head of income from house property.

- Schedule BP: Computation of income from business or profession.

- Schedule-CG: Calculation of income from capital gains.

- Schedule 112A: Details of capital gains where section 112A is applicable.

- Schedule 115AD (1) (b) (iii) Proviso: Capital gains details for non-residents where section 112A is applicable.

- Schedule OS: Calculation of income from other sources.

- Schedule-CYLA: Income statement after set-off of current year's losses.

- Schedule CYLA-BFLA: Statement of income after set-off of current year's losses and unabsorbed losses brought forward from past years.

- Schedule CFL: Statement of losses to be carried forward to future years.

- Schedule-DPM: Calculation of depreciation on plant and machinery under the Income Tax Act.

- Schedule DOA: Computation of depreciation on other assets under the Income Tax Act.

- Schedule DEP: Summary of depreciation on all the assets under the Income Tax Act.

- Schedule DCG: Calculation of deemed capital gains on the sale of depreciable assets.

- Schedule FSI: Details of income from outside India, as well as tax relief.

- Schedule TR: Statement of tax relief claimed under Section 90, Section 90A, or Section 91.

Business Codes Applicable for ITR-3 Filing

These codes will be applicable if the individual or NRI has a business, profession, or income-generating activity in India under ITR-3:

| Category | Business/Profession/Service Description | Code |

|---|---|---|

| Real Estate and Investment Related (if applicable to business) | Commercial banks, savings banks, and discount houses | 13001 |

| Housing finance activities | 13005 | |

| Credit cards | 13007 | |

| Mutual funds | 13008 | |

| Life insurance | 13011 | |

| Pension funding | 13012 | |

| Non-life insurance | 13013 | |

| Administration of financial markets | 13014 | |

| Stock brokers, sub-brokers, and related activities | 13015 | |

| Financial Intermediation Services | Finance advisers, mortgage advisers, and brokers | 13016 |

| Foreign exchange services | 13017 | |

| Other financial intermediation services n.e.c. | 13018 | |

| Investment activities | 13010 | |

| Computer and Related Services | Software development | 14001 |

| Other software consultancy | 14002 | |

| Data processing | 14003 | |

| Other IT-enabled services | 14005 | |

| BPO services | 14006 | |

| Cyber cafe | 14007 | |

| Maintenance and repair of office, accounting, and computing machinery | 14008 | |

| Computer training and educational institutes | 14009 | |

| Professions (Freelance or Consulting) | Legal profession | 16001 |

| Accounting, bookkeeping, and auditing profession | 16002 | |

| Tax consultancy | 16003 | |

| Architectural profession | 16004 | |

| Engineering and technical consultancy | 16005 | |

| Advertising | 16006 | |

| Fashion designing | 16007 | |

| Interior decoration | 16008 | |

| Market research and public opinion polling | 16012 | |

| Business and management consultancy activities | 16013 | |

| Labour recruitment and provision of personnel | 16014 | |

| Investigation and security services | 16015 | |

| Building-cleaning and industrial cleaning | 16016 | |

| Packaging activities | 16017 | |

| Medical profession | 160191_1 | |

| Film artist | 16020 | |

| Other professional services n.e.c. | 16019 | |

| Other Services | Hair dressing and other beauty treatments | 21001 |

| Event management | 21008_01 | |

| Other services n.e.c. | 21008 |

Common NRI Categories Required to File ITR-3

When NRIs select the nature of business or profession code while filing ITR-3, these are the most commonly used categories:

- 14001: Software development

- 16002: Accounting, bookkeeping, and auditing profession

- 13010: Investment activities

- 13014: Administration of financial markets

- 13016: Financial advisers, mortgage advisers, and brokers

- 16013: Business and management consultancy activities

Key Changes in ITR-3: AY 2023-24 vs AY 2024-25

The changes below have been added in the ITR-3 form of the FY 2022-2023 (AY 2023-2024) and are applicable for FY 2023-2024 (AY 2024-2025) as well:

- As an additional disclosure measure, foreign institutional investors (FI/FPI) are required to provide their SEBI registration number.

- Turnover and income from intraday trading should be reported under the newly introduced section, "Trading Account."

- A new Schedule VDA has been incorporated to report your income separately from crypto and other VDAs. If you treat income from VDAs as capital gains, you will have to provide a quarterly breakdown under the capital gains schedule. As per the ITR-3 amendments, every VDA transaction must be reported along with the sale and purchase dates.

To Conclude

Having a good understanding of who must file an ITR-3, what information it requires, and the latest updates for the current tax season is vital to ensure tax compliance and a smooth, informed tax filing experience. Whether you are a freelancer, small business owner, or professional with a private practice, learning the dos and don'ts of ITR-3 can ease the tax filing process. In this blog, we have covered everything that will help you enhance your tax returns and understand the requirements for Income Tax for NRIs. From learning about the applicable sections of ITR-3 for NRIs to the process of filing it online, we have covered everything. However, if you are still worried or confused about the application process, contact the experts at Savetaxs.

Our experts have more than a decade of experience and will ensure that all your tax-related issues are resolved, as they have the required knowledge and expertise. They are working around the clock to help you avoid any stress. Therefore, choosing Savetaxs will help you get the best guidance and assistance from the industry's top experts.

Speak to our experts and get personalized solutions for your NRI tax needs

View Plan- What are the 5 Heads of Income Tax?

- What Is Form 16? Meaning, Components & Download Guide (FY 2024-25)

- Late Filing Fee & Penalty for ITR in India (AY 2025-26) – Due Dates, Belated Return Guide

- Advance Tax Planning for NRIs: How to Pay & Claim Refunds in India

- Form ITR-V: How to Download Your ITR-V from the Income Tax Portal?

- NRI Income Tax in India (2025): Rules, Slabs, Capital Gains & ITR Forms

- What is ITR-U (Updated Income Tax Return) for NRIs?

- Capital Gains and its Taxability For NRIs in India

- ITR-2 for NRIs: Eligibility, Documents & Filing for FY 2024-25 (AY 2025-26)

- Income Tax Notice Explained: Types, Reasons & How to Respond

Mr Shaw brings 8 years of experience in auditing and taxation. He has a deep understanding of disciplinary regulations and delivers comprehensive auditing services to businesses and individuals. From financial auditing to tax planning, risk assessment, and financial reporting. Mr Shaw's expertise is impeccable.

Frequently Asked Questions

The ITR-3 form is now available for all taxpayers. The Income Tax Department has already released the utility for ITR-2 and ITR-3 on the 11th of July, 2025.

If you don't file ITR-3 within the due date for AY (Assessment Year) 2025-2026, you might attract a penalty. The penalty can be up to Rs. 1,000 for individuals who have an income of nearly Rs. 5,00,000 and a penalty of Rs. 5,000 for individuals who have an income of more than Rs. 5,00,000. You can file a belated return by the 31st of December for not filing the return within the due date. However, this will attract interest on the due amount of tax at the rate of 1% every month.

Yes, you can file ITR-3 without the help of a CA. However, it is advised to seek help from a professional while filing returns if you don't have a good understanding of income tax, to avoid making mistakes while filing the return. If you file your return yourself without being aware of the IT rules, then some benefits might remain unclaimed. Instead, the experts at Savetaxs can deal with these issues, and they have all the required knowledge and expertise.

Currently, there are seven types of ITR notified by the department, each catering to a specific type of taxpayer, i.e., ITR-1, ITR-2, ITR-3, ITR-4, ITR-5, ITR-6, and ITR-7.

A salaried person must file ITR-3 if they also have business or professional income, such as freelancing, consulting, or income from a partnership. They can file ITR-3 by following the steps below: 1 . Report salary under Income from salary, 2. Report the income from business or professional under the Profits and Gains of Business or Profession section, 3 . Claim business and deductions as per eligibility, 4 . File the ITR-3 online via the official portal of Income Tax, or utilise an online platform specified for tax filing, 5. E-verify your return using Aadhaar OTP, net banking, or simply by sending ITR-V.