How NRIs can e-verify IT Return From Abroad?

Read More

It is a critical responsibility of every taxpayer in India to file their Income Tax Return on time. Filing it on time not only ensures tax law compliance but also helps you claim or receive refunds, thereby avoiding any legal trouble. But if you fail to do so, obligations and other legal consequences are waiting at the door.

This blog will discuss the late filing fee and penalty for failing to file your ITR by the due date.

The due date to file your income tax return (ITR) in India is generally 31 July for non-audited cases and 31 October for audited cases, unless extended by the government. These dates apply to residents, non-resident Indians (NRIs), OCI cardholders, and HUFs where applicable.

Now that the new tax regime has been introduced, there are two tax regimes, old and new. Also you can choose either based on your suitability while filing your income tax returns.

However, ensure that the new tax regime is set as the default for ITR filing. Unless you specifically select the old tax regime, the new tax regime will apply by default. Ensure that you file your ITR before the due date; otherwise, the Income Tax Act may impose penalties on taxpayers.

Individuals, NRIs, OCI cardholders, or HUFs whose income exceeds the basic exemption limit (₹2.5 lakh under the old regime or ₹3 lakh under the new regime) or who meet other specified conditions under the Income Tax Act are required to file an Income Tax Return (ITR).

| Income Tax Slab | Old Regime Income Tax Rate | Surcharge |

|---|---|---|

| Up to ₹2,50,000 | Nil | Nil |

| ₹2,50,001 – ₹5,00,000 | 5% above ₹2,50,000 | Nil |

| ₹5,00,001 – ₹10,00,000 | ₹12,500 + 20% above ₹5,00,000 | Nil |

| ₹10,00,001 – ₹50,00,000 | ₹1,12,500 + 30% above ₹10,00,000 | Nil |

| ₹50,00,001 – ₹1,00,00,000 | ₹1,12,500 + 30% above ₹10,00,000 | 10% |

| ₹1,00,00,001 – ₹2,00,00,000 | ₹1,12,500 + 30% above ₹10,00,000 | 15% |

| ₹2,00,00,001 – ₹5,00,00,000 | ₹1,12,500 + 30% above ₹10,00,000 | 25% |

| Above ₹5,00,00,000 | ₹1,12,500 + 30% above ₹10,00,000 | 37% |

| Income Tax Slab | New Regime Income Tax Rate | Surcharge |

|---|---|---|

| Up to ₹3,00,000 | Nil | Nil |

| ₹3,00,001 – ₹7,00,000 | 5% above ₹3,00,000 | Nil |

| ₹7,00,001 – ₹10,00,000 | ₹20,000 + 10% above ₹7,00,000 | Nil |

| ₹10,00,001 – ₹12,00,000 | ₹50,000 + 15% above ₹10,00,000 | Nil |

| ₹12,00,001 – ₹15,00,000 | ₹80,000 + 20% above ₹12,00,000 | Nil |

| ₹15,00,001 – ₹50,00,000 | ₹1,40,000 + 30% above ₹15,00,000 | Nil |

| ₹50,00,001 – ₹1,00,00,000 | ₹1,40,000 + 30% above ₹15,00,000 | 10% |

| ₹1,00,00,001 – ₹2,00,00,000 | ₹1,40,000 + 30% above ₹15,00,000 | 15% |

| Above ₹2,00,00,001 | ₹1,40,000 + 30% above ₹15,00,000 | 25% |

Please note that the surcharge of 25% to 37% is not imposed on income chargeable under Sections 111A, 112, 112A, and dividend income. The maximum surcharge on such income is generally 15%, except where specific provisions like Sections 115A, 115AB, 115AC, 115ACA, and 115E apply.

If you miss the due date, the government allows you to file a belated income tax return by 31 December of the relevant assessment year. Under Section 234F, filing your income tax return after the due date can attract a late fee of up to ₹5,000. If your total income is below ₹5 lakh, the late fee is restricted to ₹1,000.

No late filing fee applies if your income is below the basic exemption limit.

If a taxpayer fails to file their income tax return before the due date, they can still file it by 31 December of the assessment year. This is called a belated return under Section 139(4) of the Income Tax Act. However, it may attract penalties and certain restrictions.

As mentioned above, filing a belated income tax return can result in fines and disadvantages. Here is what happens:

Interest Penalties: Interest may be charged under Sections 234A, 234B, and 234C, increasing your tax liability.

Last Fees:

Under Section 234F:

Limitations on Loss Carry Forward: If you file your income tax return after the due date, you generally cannot carry forward certain losses such as business losses or capital losses to future years. However, loss under the head “Income from House Property” can still be carried forward even if the return is filed late. Unabsorbed depreciation may also be carried forward as per applicable provisions.

No deductions and Exemptions: If an Individual files their ITR on time, they are eligible for certain tax benefits under sections 10A, 10B, 80-IA, 80-IB, 80-IC, 80-ID, and 80-IE. Late filing of your ITR means you will not be eligible for any tax benefits, which will ultimately increase your tax burden.

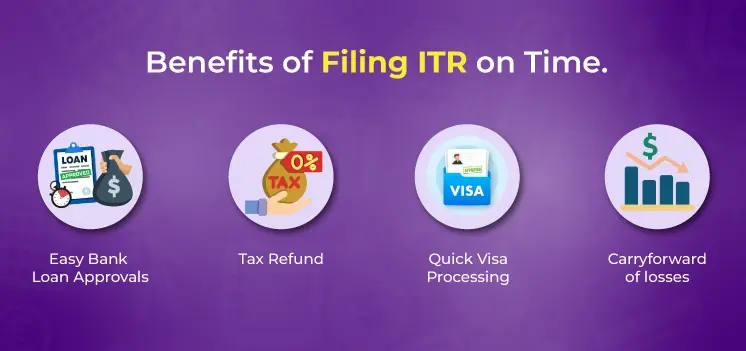

Filing ITR on time comes with endless benefits, which include:

When applying for a bank loan, financial institutions and banks require a copy of your ITR as proof of your financial standing. If you file an ITR on time, you will be perceived as a responsible taxpayer in India with a stable income, which makes it easier for banks to approve your loan.

As a taxpayer, if you have overpaid your taxes, you are eligible to claim a refund by filing your return on time. The sooner you file, the earlier you will receive your refund.

Some countries require you to submit a copy of your ITR while applying for a visa. Now, timely filing of ITR ensures that your return is processed quickly and without any delay.

If you file your ITR on time or before the due date, you can set those losses from your business or profession against your income in the same or subsequent years. This will also help you reduce your tax liability.

Filing ITR as an NRI in India can feel overwhelming. Indian tax laws can feel like an unsolved puzzle, leaving you with no clear understanding. Well, not anymore. SaveTaxs has been helping NRIs for decades in filing their ITR. Our satisfied client base of thousands of NRIs, along with our team of experts, is a testament to the quality of services we offer.

We provide NRIs with an NRI-specific ITR strategy, ensuring that we minimize your taxability. Hence, no matter where you are in the world, we work 24/7 across all times so that you can file your ITR from anywhere, at any time.

Connect with us now before the ITR deadlines hit.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr Varun is a tax expert with over 13 years of experience in US taxation, accounting, bookkeeping, and payroll. Mr Gupta has not prepared and reviewed over 5000 individual and corporate tax returns for CPA firms and businesses.

Want to read more? Explore Blogs