Your Complete Guide on EPF Withdrawal for NRIs

Read More

As an NRI business owner in India, you generally should file ITR-3 if you have income from a profession or business as an individual or an HUF. However, the income tax department has various ITR forms, each serving a different type of taxpayer with business income. Choosing the right ITR form as a business owner is essential as it ensures a fast process, accurate tax compliance, and avoids unnecessary notices from the department.

In this blog, we will understand which ITR form you should file for business income in India

The following are the ITR forms for NRI business owners.

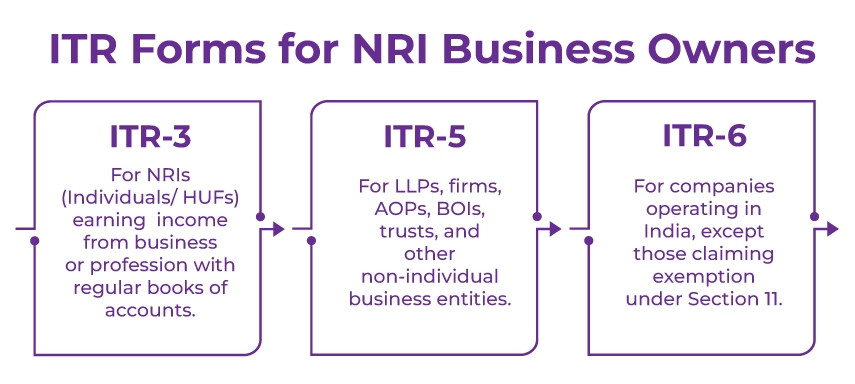

ITR-3 is the income tax return form for individuals and HUFs with income from a business or profession. This form is applicable when the concerned NRI taxpayer maintains the regular books of account and the total business income exceeds the threshold of Rs 50 lakhs.

Who Shall File ITR-3

The income tax filing form ITR-5 is used by LLPs (Limited Liability Partnerships), AOPs (Associations of Persons), BOIs (Bodies of Individuals), AJP (Artificial Juridical Person), Estates of deceased and insolvent persons, Business trusts, and investment funds.

Who Shall File the ITR-5 Form

ITR Form 6 is specifically for companies. However, ITR-6 is not applicable for a company engaged in charitable activities or eligible for exemption under section 11.

Who Shall File ITR-6

Companies registered under the Companies Act 2013 or the earlier Companies Act 1956 must file the ITR 6 form. But if the company incurs or receives proceeds from property that is held for religious or charitable purposes, it shall not be liable for ITR 6.

The following table outlines the criteria, situations, and the applicable ITR form for NRI business owners.

|

Criteria |

Situation |

Applicable ITR Form For NRI Business Owner |

|---|---|---|

|

Nature of Income |

Business or professional income |

ITR-3 |

|

No business income (only capital gains, rent, or interest) |

ITR-2 |

|

|

Business Structure |

Individual/ Sole Proprietor. |

ITR-3 |

|

Partnership Firm/LLP |

ITR-5 (filed by entity) |

|

|

Company (Private Ltd / One Person Company (OPC)) |

ITR-6 (filed by company) |

|

|

Income Complexity |

Multiple income sources + business income. |

ITR-3 |

|

Simple income without a business. |

ITR-2 |

|

|

Compliance Requirement |

Tax audit applicable |

ITR- 3 (with an audit report) |

|

No audit requirement |

ITR-2 or ITR-3 (based on income type) |

Compliance requirements in India go beyond merely filing the ITR form for an NRI business owner. This involves maintaining proper financial discipline, adhering to regulatory timelines, and ensuring accurate income reporting.

The following is the key compliance requirement that every NRI business owner should follow.

The following are the common mistakes NRI business owners must avoid while filing their returns.

Savetaxs experts provide clear guidance for your Indian business journey.

Filing ITR as an NRI business owner isn't complex as long as you have chosen the right ITR form and maintain compliance throughout the ITR filing process. Using the correct ITR form ensures faster refunds and easy compliance.

As an NRI business owner in India, if you are seeking professional guidance in filing an income tax return, Savetaxs is the name to trust. We provided tax advisory and planning services to NRIs and OCIs earning professional business or entrepreneurial income in India.

From residential status determination to income tax return filing, TDS and AIS/Form 26AS reconciliation, double taxation avoidance agreement advisory, FEMA/RBI compliance, and more, our team of experts helps you with every aspect of your ITR filing as an NRI business owner.

Connect with us as we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr. Ritesh has 20 years of experience in taxation, accounting, business planning, organizational structuring, international trade financing, acquisitions, legal and secretarial services, MIS development, and a host of other areas. Mr Jain is a powerhouse of all things taxation.

Want to read more? Explore Blogs