Company Registration Process For NRIs In India - A Complete Guide

Read More

Minimum Alternate Tax (MAT) is a direct tax imposed on all companies if their tax liability is less than 15% of their book profits. It is a provision introduced under Section 115JB of the IT Act to ensure companies having significant book profits pay a minimum amount of tax. It primarily applies if they claim deductions, exemptions, or incentives to reduce their tax obligation. MAT is calculated based on the company's book profit, which is derived from its profit and loss account.

There are certain businesses where the MAT provisions may not apply, such as companies choosing a certain concessional tax regime, specific entities operating in designated financial service centers, etc. MAT calculation is done by calculating the book profit, applying the MAT rate, and comparing the MAT and regular tax.

Additionally, in case a company's liability is more than its regular tax liability, it can avail the benefit of the MAT credit. Excess MAT paid can be carried forward for up to 15 assessment years. In this blog, we will cover everything related to Minimum Alternative Tax (MAT).

Minimum Alternative Tax (MAT) is a provision introduced under Section 115JB of the Income Tax Act of India. It ensures companies with significant book profits pay a minimum amount of tax, even if they claim deductions, exemptions, or incentives to reduce their tax liability.

MAT is a direct tax imposed on all companies, including foreign companies. Rather than the company's taxable income, it is calculated based on the company's book profit, which is derived from its profit and loss account. MAT applies if a company's tax liability is less than 15% of its book profits, and the company needs to pay tax at the specified rate.

Every company registered in India, including foreign companies, is responsible for paying MAT under Section 115JB. The company will have to pay advance tax, and it will be subject to penalties if it hides the income. Previously, MAT didn't apply to companies earning profits in Special Economic Zones (SEZs).

However, later, when the laws were amended, MAT became applicable to all such companies that operate in SEZs. Every company needs to submit a report from a certified CA stating that the book profit has been computed under Section 115JB.

Although MAT applies to many companies, certain businesses may not fall under the provisions of MAT. Here are some situations when MAT may not apply:

These alternative tax regimes often require companies to give up certain deductions and incentives in exchange for lower tax rates.

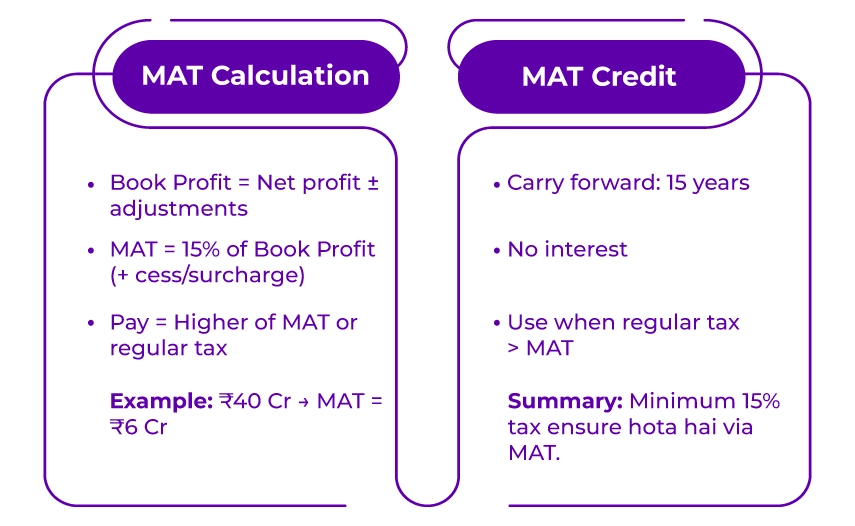

Follow the steps below accurately for the Minimum Alternate Tax calculation, which involves determining the company's book profit and applying the prescribed tax rate:

According to the latest tax regulations, the current MAT rate is set at 15% of the book profit. A surcharge and cess for health and education may also apply, based on the company's level of income.

Based on the regular provisions of the Income Tax Act, calculate the tax liability. The company will have to pay MAT if the MAT amount is higher.

For example, suppose a company's book profit is Rs. 40 crore, the MAT liability will be calculated:

When a company's liability exceeds its regular tax liability, it can avail itself of the MAT credit benefit. Under the regular provisions of the Income Tax Act, the excess MAT paid can be carried forward and set off against future tax liabilities. Keep the following features of MAT credit in mind:

Minimum Alternate Tax is an important factor for NRIs who own a business in India. Many NRIs invest in Indian businesses via private limited companies or joint ventures. Such companies often avail of deductions like:

Since MAT tax is calculated based on book profits, MAT provisions may still apply even when these deductions reduce tax liability significantly.

Here are some important points to keep in mind for NRIs owning businesses in India:

Additionally, NRIs must consider international tax planning, especially if their company profits are distributed as dividends or repatriated abroad.

For businesses operating in India, understanding the implications of MAT under Section 115JB of the IT Act is important. It is designed to ensure that companies pay a minimum corporate tax, even when deductions and exemptions significantly reduce their tax liability. The MAT calculation is done based on the book profits instead of the company's taxable income.

Additionally, to better understand the implications of MAT, seek guidance from an expert at Savetaxs. We have an entire team of experts who can guide you through everything related to the Minimum Alternate Tax. Our team can help you submit all the necessary reports to ensure 100% accuracy with the rules. Contact us right away as we are actively working 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr. Ritesh has 20 years of experience in taxation, accounting, business planning, organizational structuring, international trade financing, acquisitions, legal and secretarial services, MIS development, and a host of other areas. Mr Jain is a powerhouse of all things taxation.

Want to read more? Explore Blogs

_1772791127967.webp&w=828&q=75)

_1772887385012.webp&w=828&q=75)

_1773060834347.webp&w=828&q=75)