How Is NRE Account Taxed In India?

Read More

Every NRI running a business in India has thought about this one question: "What bank account should I use for business transactions?" Well, the answer depends on multiple factors because a bank can directly impact your taxation, compliance, and ease of managing funds across borders.

In India, the financial system for NRIs is governed by FEMA regulations, which state how income can be earned, repatriated, or held. Using an incorrect or non-compliant account can lead to issues, penalties, or restrictions during fund transfers. Henceforth, selecting the right bank account is necessary for smooth and lawful business operations.

In this blog, we will answer the most frequently asked question among NRI business owners: "Which bank account is best for NRI business?"

As an NRI business owner in India, selecting the right bank account depends on the nature of income and the business structure. The following table provides a quick comparison to help you determine which bank account an NRI should use for business transactions.

| The Account Type | Best For | Can It Be Used For Business? | Repatriation | Recommendation |

|---|---|---|---|---|

| NRO Account | Income earned in India | Yes | Limited to USD 1 million/year. |

Best for most NRIs.

|

| NRE Account | Foreign Income | Not suitable for Indian business income | Fully repatriable |

Use for savings and transfers.

|

| Current Account | Companies /LLPs | Yes | Depends on the structure |

Required for entities.

|

The aforementioned table clearly demonstrates that the NRO account and the NRI current account are the most relevant and appropriate options for the bank account an NRI must use for business transactions

Connect with Savetaxs, and get the best NRI banking services as per your financial and investment goals from the experts.

For NRI business owners earning business income in India, having an NRO (Non-Resident Ordinary) account is the most practical choice.

NRO account for NRIs is ideal in the following ways:

The NRO account limitation affects the NRI repatriation process. The repatriation of funds through the NRO is limited to USD 1 million per financial year.

Note: For professionals, freelancers, consultants, and individual entrepreneurs, the NRO Account is the most suitable option when deciding which bank account NRIs should use for business transactions.

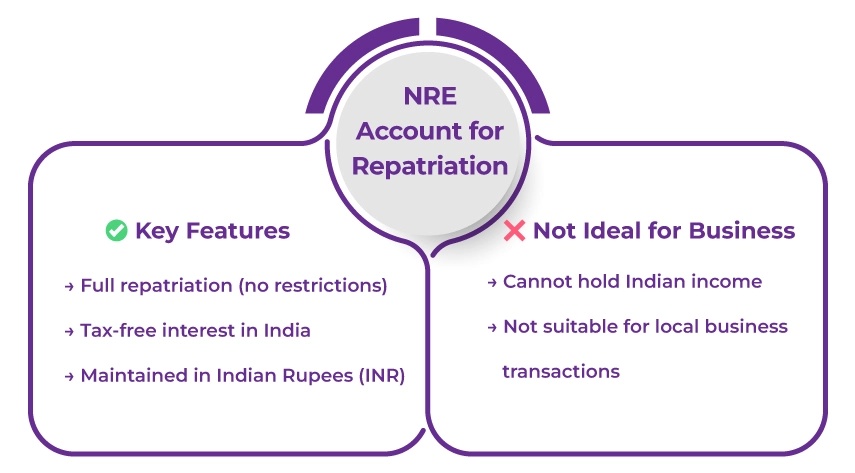

The NRE (Non-Resident External) Account is designed for managing foreign income. NRIs can use an NRE Account to park their foreign earnings in India.

As an NRI business owner, if you run a registered business in India as a company or LLP, having a current account becomes essential.

A current account supports unlimited transactions. The ticket size for international transactions is much larger than for local businesses. Hence, your current account ensures there is no cap on transaction amounts. Furthermore, as an NRI business owner, you can facilitate as many transactions in a month as you want.

The current accounts further facilitate payroll, vendor payments, and operational expenses.

However, please ensure that, as part of FEMA and RBI regulatory compliance, NRIs in India cannot operate a regular savings account to conduct their business transactions. Hence, NRIs must use a special current account, such as an NRE Current Account or an NRO Current Account.

Additionally, the account must be opened in the business entity's name.

The following table demonstrates the factors to consider while selecting the right account for your business model and financial needs.

|

Nature of Income |

Income earned in India |

NRO Account |

|

Income earned abroad |

NRE Account |

|

|

Type of business |

Freelancer/consultant |

NRO Account |

|

Company/LLP |

Current Account |

|

|

Repatriation Needs |

Frequent Transfer Abroad |

NRO + NRE Account |

|

Limited Transfer |

NRO account |

|

|

Transactions Volume |

Low transactions |

NRO Account |

|

High transactions |

Current Account |

Choosing the right bank account ensures both regulatory compliance and operational efficiency.

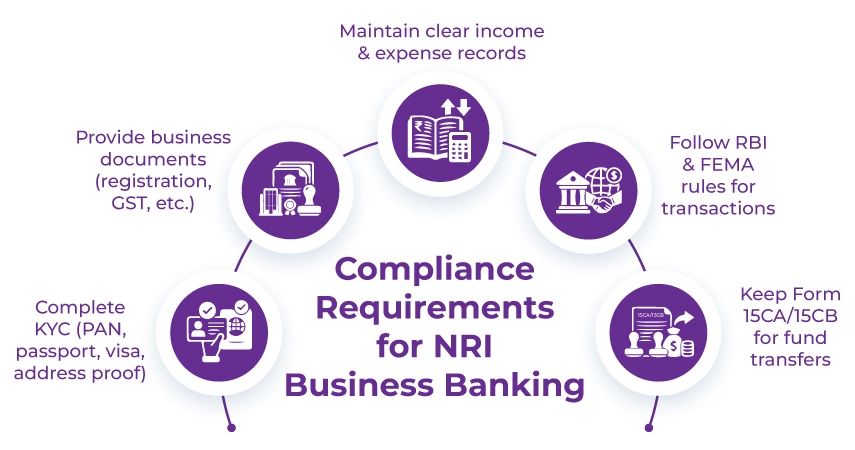

The following are certain compliance requirements that an NRI must adhere to when managing business transactions in India.

In a nutshell, as an NRI business owner running a business in India, if your documents are correct, your records are clear, and you follow the RBI rules, you are certainly safe from any legal complications ahead.

While running a business in India as an NRI, there are certain mistakes NRIs make without realizing, and these mistakes can cause problems later. Here are the following mistakes that you shall avoid.

Savetaxs expert guidance provides procedural support for investments and ventures in India.

As an NRI running a business in India, choosing the correct banking structure is essential. However, the answer to which bank account NRIs must use for business transactions depends on the business structure and the source of income. However, here is a quick summary of NRI business bank accounts in India.

NRIs, you shall understand the importance of a well-managed banking setup, as it ensures efficient fund management across all your business activities, compliance, and hassle-free operations.

As an NRI, if you are seeking to open an NRI-centric bank account in India and are seeking professional assistance for the same, Savetaxs is the name to trust. Our expertise here provides end-to-end consultation to guide your thought process or the physical account-opening journey, including filing the relevant application form with the bank. Additionally, you also get expert consultation on KYC verification, document management, remittances, investments, and more, ensuring 100% compliance with FEMA and RBI regulations throughout the process.

Connect with us as we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr Varun is a tax expert with over 13 years of experience in US taxation, accounting, bookkeeping, and payroll. Mr Gupta has not prepared and reviewed over 5000 individual and corporate tax returns for CPA firms and businesses.

Want to read more? Explore Blogs

_1771496574280.webp&w=828&q=75)

_1771836712958.webp&w=828&q=75)

_1771851103775.webp&w=828&q=75)