_1769758257.webp&w=828&q=75)

What Is a Non-Repatriable Demat Account?

Read More

_1772531140227.png&w=3840&q=75)

NRO accounts help NRIs to handle their income earned in India, but they come with certain tax implications, such as TDS on interest and other earnings. Considering this, knowing the account rules, repatriation limits, and minimum balance makes it simple for NRIs to manage their money. Additionally, with proper tax planning, they can reduce their tax burden and get more out of their NRI accounts.

Further, to help you out, this blog explains the tax implications on NRO account for NRIs in India. It includes the types of income taxes, applicable rates of taxes, and how NRIs can benefit from DTAA to claim tax credit. So read on and gather all the information.

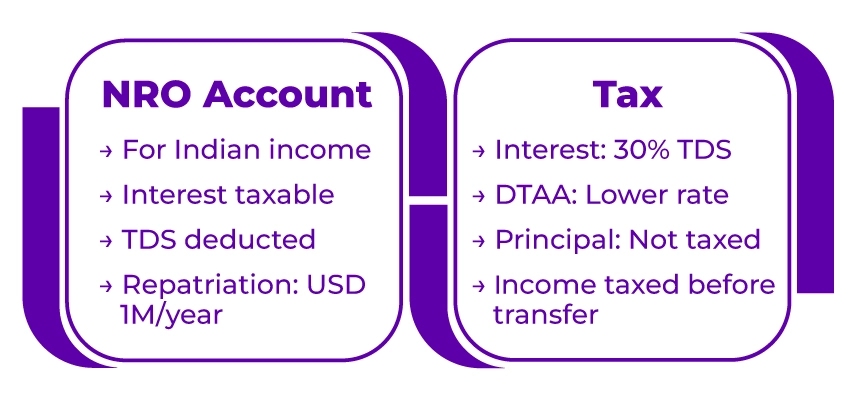

An NRO or Non-Resident Ordinary account is a bank account designed for NRIs to manage earned income in India. It includes pensions, capital gains, rent, or dividends. In this account, NRIs can deposit both funds, i.e., obtained from Indian and foreign sources, making it a flexible savings account. Income deposited in this account is subject to Indian tax laws and is taxable in India. Considering this, the bank deducts Tax Deducted at Source (TDS) on interest and other earnings from the NRO account.

Apart from this, per financial year, NRIs can repatriate a maximum of USD 1 million from their NRO account. However, before this, NRIs need to pay the necessary taxes. Further, an NRO account is a flexible option for NRIs to manage their Indian income while living overseas.

This was all about the NRO account. Moving ahead, let's know the tax on NRO account.

To maximize savings and avoid surprises, it is vital for NRIs to understand the taxation rules of NRO accounts. To help you out, here is a breakdown of tax implications on an NRO account:

So, this was all about the tax implications of an NRO account. Moving further, let's know the benefits of having an NRO account for an NRI.

Here are the benefits of having an NRO account for an NRI:

These are some of the benefits of having an NRO account for an NRI. Moving ahead, let's know the restrictions of an NRO account.

Apart from benefits, NRO accounts do have some limitations. These are as follows:

This was all about the restrictions of an NRO account. Moving further, let's know the documents required to open an NRO account in India.

NRIs need to submit the following documents to open an NRO account:

These are the documents NRIs generally need to open an NRO account.

Connect with Savetaxs and, with the expert guidance, simplify your NRI taxes today.

Lastly, to effectively manage your India-based income while living overseas, it is vital to understand the tax implications on the NRO account, its repatriation limits, and associated tax exemptions. It helps you to stay compliant and make the right decisions.

Further, if you are facing issues in managing your Indian income and seeking guidance, connect with Savetaxs. We have a team of financial experts who can help you make informed and wise decisions. Additionally, assist you in optimizing your financial strategies to manage your NRO accounts.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr. Ritesh has 20 years of experience in taxation, accounting, business planning, organizational structuring, international trade financing, acquisitions, legal and secretarial services, MIS development, and a host of other areas. Mr Jain is a powerhouse of all things taxation.

Want to read more? Explore Blogs