NRI Repatriate Profits From Indian Business - Process, Rules & More

Read More

Starting a business in a fast-growing entrepreneurial landscape of India is exciting. However, it comes with a long list of legal responsibilities. In this, annual compliances are mandatory financial and legal filings for registered businesses. It ensures legitimacy and transparency. As a startup owner, you need to be aware of these statutory and regulatory requirements. Hence, to avoid penalties, follow the annual compliance checklist for startups. These are regulated by the Companies Act 2013 and various guidelines stated by FEMA, RBI, and SEBI.

Further, to help you out, this blog provides a detailed annual compliance checklist for startups in India. So read on and gather all the information.

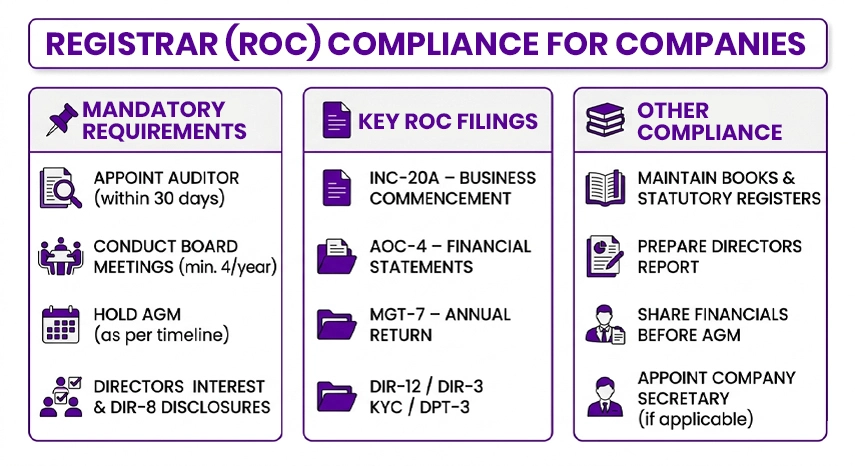

Registrar-based compliances are also known as mandatory compliances. These are certain compliance requirements that need to be mandatorily adhered to, and the requisite information provided to the Registrar of Companies (ROC). It can be submitted at the end of each financial year or on the occasion of specific events. For instance, changes in the Memorandum of Association (MOA) or the Articles of Association (AOA), changes in share capital, or changing or appointing a director in a company. Further, register-related compliance includes:

According to Section 139 of the Companies Act, 2013, it is mandatory to appoint a statutory auditor within 30 days of the incorporation of a company. The statutory auditor should be appointed at the board meeting. Additionally, other auditors must be appointed at the Annual General Meeting (AGM) by filing Form ADT-1 within 15 days of the AGM. Further, the auditor is appointed for a term of five years, and annual ratification is no longer mandatory unless specifically required by the company.

Section 173 of the Companies Act, 2013 states that within 30 days of incorporation, the company should conduct its first board meeting. Additionally, it should organize a minimum of four board meetings in every financial year. Also, the gap between each board meeting should not be more than 90 days.

According to Section 96 of the Companies Act, 2013, after incorporation of the company, the first AGM should be held within 9 months from the end of the first financial year. Additionally, the subsequent AGMs should be held within 6 months of the end of the financial year. Considering this, between the two AGMs, the gap should not be more than 15 months. Apart from this, the notice of these meetings should be sent to all statutory auditors, directors, and members.

As per section 184(1) of the Companies Act, 2013, every company director needs to disclose their interest in the first board meeting of the director in each financial year. Considering this, if there is a change in the interest of the directors, they need to fill out Form MBP-1.

With Savetaxs, get professional guidance on your tax obligations and maximize your refunds.

According to section 164(2) of the Companies Act, 2013, every director needs to file a disclosure of non-disqualification in Form DIR-8. The purpose of it is to confirm that the director is not disqualified from his position. Further, the disclosure is required annually, generally, at the first board meeting of every financial year.

The e-form filings with the ROC are as follows:

Under section 134 of the Companies Act 2013, the Directors' Report should be filed covering all the details required for a Small Company. The report should be signed "Chairperson" if authorized by the Board or by at least two directors if the chairperson is not authorized. Here, one should have a managing director. In the case of a one-person company, the report is signed by one director.

According to sections 128 and 88 of the Companies Act 2013, every company needs to update and maintain certain records for the inspection of the ROC, like:

The company, at least 21 days before the AGM, should send the members of the company the approved director's report, financial statements, and auditor's report.

As per section 203 of the Companies Act 2013, every company whose paid-up share capital is INR 5 crore or more should appoint a whole-time company secretary.

This was all about the registrar-based annual compliance checklist for startups. Other compliance of such companies includes periodic tax filing and other returns. Additionally, maintenance of accounts under the Income Tax Act and other statutes as applicable. Further, from case to case, depending upon the nature of the business, offered services or products, net worth, the turnover value, borrowings, and more, the compliance requirements differ.

Moving ahead, let's know the non-registrar-based annual compliance checklist for startups.

Some annual compliance checklists for startups are not mandated by the ROC. However, due to other existing rules and regulations, they need to be followed. These include:

Further, NRIs with FEMA compliance NRI startups also need to follow these tax compliance requirements when starting a business in India. Considering this, often NRI entrepreneurs get overwhelmed by various compliances and, in the absence of expert guidance, end up paying penalties. Considering this, to avoid any hassle and stay updated with the annual compliance checklist for startups, it is advisable for NRIs to take professional guidance.

Moving further, let's know about the penalties for non-compliance with the ROC.

The companies should ensure that all the mandatory compliances are filed with the ROC. In case they fail to do so, they are liable to pay a heavy penalty based on the number of compliance items they missed. Penalties for non-compliance are generally levied on a per-day basis (commonly ₹100 per day for many ROC forms) and may vary depending on the specific form and delay period. Moreover, the penalty cost is increased to INR 200 per day by the Ministry of Corporate Affairs (MCA). Previously, it was INR 100 per day.

Additionally, if companies fail to complete all the compliances, the digital signature of the company's director is suspended. It is activated only if complete compliance and penalties are paid. Further, in cases of prolonged non-compliance, the Director Identification Number (DIN) may be deactivated, restricting access to MCA filings until compliance is completed. Also, in certain situations, the directors of the companies may be charged and imprisoned.

Note: The above-mentioned registrar and non-registrar related compliance is for private limited companies. It is specifically for small companies whose paid-up capital is up to ₹4 crore and having an annual turnover of up to ₹40 crore, as per the latest MCA thresholds.

Connect with Savetaxs and let our experts take care of all your startup compliance

Lastly, compliance is often considered a burden by startups. However, it is an important foundation for long-term business success. Considering this, following the annual compliance checklist for startups helps NRI businesses to safeguard assets, avoid penalties, and build a reputable brand. By adhering to these guidelines, startups can focus on growth knowing that their business is operationally and legally secure.

Further, if you need professional assistance, feel free to connect with Savetaxs. Our financial experts will guide you at every step and make compliance easy. We are 24/7 available to help NRIs with business and tax assistance in India.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr Varun is a tax expert with over 13 years of experience in US taxation, accounting, bookkeeping, and payroll. Mr Gupta has not prepared and reviewed over 5000 individual and corporate tax returns for CPA firms and businesses.

Want to read more? Explore Blogs