Do NRIs Need A Resident Director In A Pvt Ltd Company

Read More

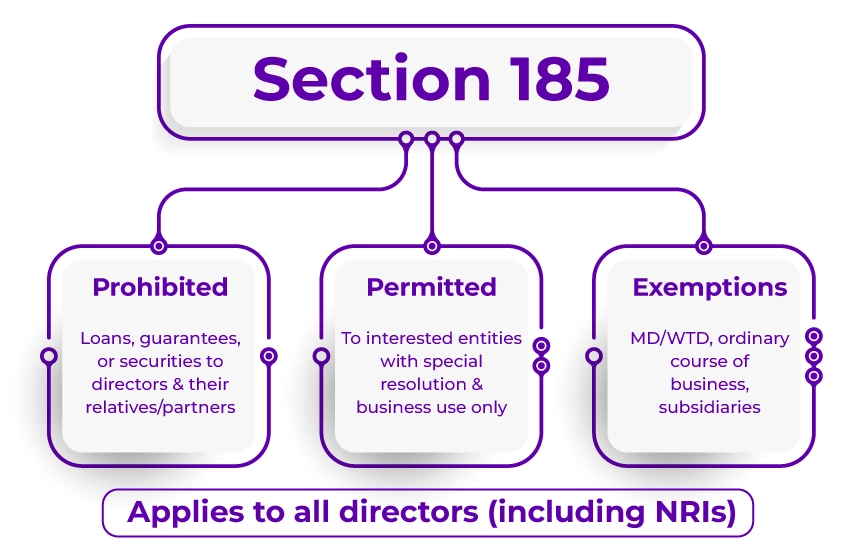

Section 185 of the Companies Act 2013 is an essential regulation that governs the financial and loan transactions between companies and their directors or related parties. It establishes the regulations and limitations for lending money to the directors. All companies registered in India must comply with the terms and conditions set out in this section before providing any security, guarantee, or loan to their directors.

Furthermore, Section 185 imposes penalties on the defaulting corporation, its officers, and its directors for violating its terms.

In this guide, we will cover all aspects related to Section 185 of the Companies Act, including loans permitted under Section 185, exemptions, applicability, penalties for non-compliance, and more.

Section 185 of the Companies Act states that a company cannot:

By a director, a director of its holding company, a relative or a partner of any director, or any firm in which a director is either a partner or a relative.

In a nutshell, Section 185 of the Companies Act 2013 forbids companies from granting loans to directors, partners, or their relatives.

Note: For NRI directors in Indian companies, the provision under Section 185 of the Companies Act remains the same.

Section 185(2) of the Companies Act permits the company to extend loans to any entity, a person in whom any of the directors are interested, provided the following conditions are fulfilled. In simpler terms, the companies can advance loans, including loans reflected in book debt, and provide security or a guarantee in connection with any loan taken by any person in whom a company director is interested.

The conditions that must be fulfilled for the companies to extend a loan or provide any security or guarantee to the person in whom the company director is interested are as follows.

1. The company is required to pass a specific resolution in a general meeting.

2. The loan granted to the borrowing company must strictly be used for its principal business activities.

3. The general meeting explanatory statement in which the resolution for extending the loan is passed must disclose.

For the aforementioned purpose, any person in whom any of the directors of the company is interested must include the following persons:

Section 185 of the Companies Act 2013 also provides an exception to the restrictions prohibiting a company from granting a loan to its directors. The company is permitted to give a guarantee, provide security, or advance loans to:

If any provision of the Act is not complied with, Section 185(4) of the Companies Act requires that a penalty be imposed. If any company extends a loan in violation of Section 185, the company will be imposed a fine of nothing less than Rs 5 lakh, which may extend to Rs 25 lakh.

The director, or any other person related to the director to whom the security, guarantee, or any loan is extended, shall be subject to imprisonment for a period of six months, a fine of up to Rs 5 lakh, which may extend to Rs 25 lakh, or both.

The following are the key points to remember under Section 185 of the Companies Act when extending loans, providing securities, or granting guarantees.

For companies to maintain strong corporate governance, accountability, transparency, and compliance with Section 185 of the Companies Act 2013 is essential. By adhering to the provisions in this section, the companies can safeguard their financial resources, build a strong foundation of trust with their stakeholders, and protect shareholders' interests. Non-compliance with the provision will subject the defaulting party to severe penalties and punishment.

As an NRI, if you are planning to register a company in India and seeking professional guidance, Savetaxs is the name to trust. Our expertise will consult NRIs with the best business strategies, regulatory requirements for the same, documentation management, handle DSC/DIN filings, filing incorporation documents, FEMA and RBI compliance consultation, and more.

Connect with us as we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr Manish is a financial professional with over 10 years of experience in strategic financial planning, performance analysis, and compliance across different sectors, including Agriculture, Pharma, Manufacturing, & Oil and Gas. Mr Prajapati has a knack for managing financial accounts, driving business growth by optimizing cost efficiency and regulatory compliance. Additionally, he has expertise in developing financial models, preparing detailed cash flow statements, and closing the balance sheets.

Want to read more? Explore Blogs