Company Registration Cost For NRIs In India

Read More

In the domain of company law and corporate governance, the roles of an Indian resident director and an NRI director are different and legally significant from each other. Being an NRI when starting a company in India, understanding the difference between an Indian resident director and an NRI director is vital. It helps in proper management and ensures compliance.

Want to know the difference between these two types of directors? The blog provides a comprehensive breakdown of the differences between the two directors. It covers legal definitions, duties, taxation, regulatory exposure, and practical implications. So read on and gather all the information.

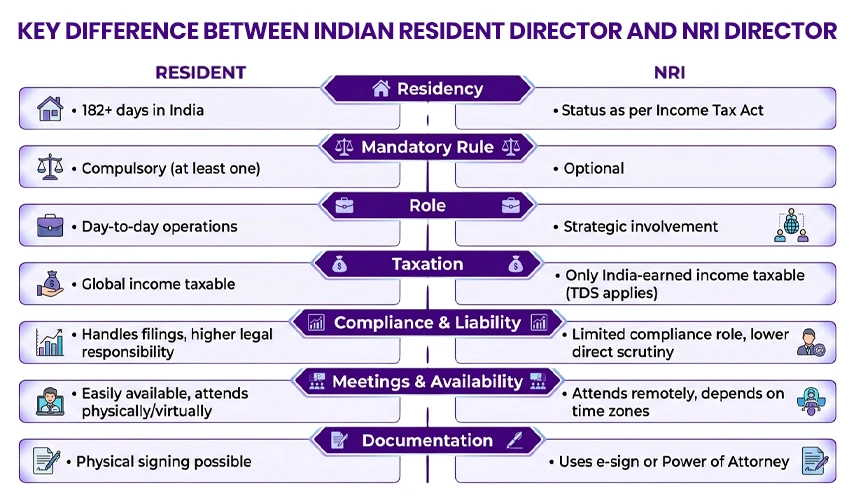

A resident director is an individual who resides in the country where the company is located. According to the Companies Act 2013, an appointed director who resides in India for 182 or more days in a previous financial year. Such a company director is known as an Indian resident director.

Further, a resident director serves as a local point of accountability. Additionally, he/she also helps in the interface of the company with government bodies, tax departments, and regulatory authorities.

This was all about an Indian resident director. Moving further, let's know about an NRI director.

A person who resides in India for less than 182 days during the preceding financial year is qualified as an non-resident India under the Income Tax Act. In simple words, an NRI director is an individual of Indian origin or citizenship who resides outside India and qualifies as a non-resident under tax laws. As per Indian law, an NRI can invest in a startup in India and also act as a director.

Additionally, the Companies Act, 2013, and the Foreign Exchange Management Act (FEMA) govern the participation of NRIs in Indian companies. NRIs holding the position of a company director in India need to follow FEMA regulations. Also, meet the other eligibility criteria, such as obtaining a Director Identification Number (DIN) and a Digital Signature Certificate (DSC).

Apart from this, NRI directors play an essential role in board-level decision-making. However, generally, they do not take part in the daily operations of the company.

So, this is what an NRI director is in an Indian company. Now, after having an overview of both the directors, let's look at the key difference between them.

The table below showcases the key differences between an Indian resident director and an NRI director.

|

Criteria |

Indian Resident Director |

Non-Resident Indian Director |

|---|---|---|

|

Definition of Residency |

Based on physical presence in the country, i.e., 182 days or more in a financial year. |

Determined based on residential status under the Income Tax Act, 1961 |

|

Mandatory Appointment |

According to the Companies Act 2013, it is mandatory to have at least one Indian resident director. |

Appointing an NRI director is not mandatory in an Indian company. |

|

Applicability |

It applies to both private and public limited companies to have an Indian resident director. |

Appointing an NRI director is an option in both public and private limited companies. It is based on expertise or need. |

|

Income Tax |

According to the Income Tax Act, 1961, the global income (Indian and foreign earnings) of Indian residents is taxable in India. |

The income of an NRI director from an Indian company is taxable if it is received or earned in India. Additionally, companies, before making payment to NRI directors for remuneration or sitting fesss also deduct tax at source (TDS). |

|

Involvement with Authorities |

Often, the primary interaction is with regulatory bodies like SEBI, ROC, and tax officials. |

Directly contacted rarely unless holding a substantial responsibility in the company. |

|

Regular Oversight |

Indian resident directors are more involved in day-to-day company matters. |

Limited involvement, generally strategic. |

|

Board Meetings |

Expected to attend either physically or virtually. |

May attend the meeting virtually from overseas. |

|

Legal Accountability |

Due to local presence, the Indian resident director may be held liable for non-compliance with the law. |

If not involved actively, the NRI director may be saved from immediate legal scrutiny. |

|

Compliance |

Expected to oversee board meetings, tax filings, and general compliance. |

Generally take part in board matters and high-level decisions. |

|

Availability for Meetings |

An Indian resident director is easily available for government liaison and local meetings. |

For NRI directors, the availability of meetings depends on remote access and time zones. |

|

Document Signing and Compliance |

Can sign physical documents and help with real-time compliance. |

For approvals, NRI directors may require an e-signature or a Power of Attorney. |

|

Ease of Communication |

Having an Indian resident director is convenient for regulators and banks. |

NRI directors, because of the location difference, may face delays. |

This is the key difference between Indian resident directors and NRI directors. Further, in India, the definition of residential director is defined based on the number of days a person is physically present in the country during a financial year. Depending on the residential status, they need to follow regulations stated under Indian tax laws and FEMA.

Moving further, let's know the legal framework governing directors in India.

Here is all the information about the legal framework governing directors in India:

This was all about the legal framework governing directors in India. It includes both Indian resident directors and NRI directors. Moving forward, let's know the advantages of having an NRI director in an Indian company.

The advantages of having NRI directors in Indian companies are as follows:

These are some of the key advantages offered by NRI directors to Indian companies. Moving ahead, in the next section, let's look at the challenges NRI directors face in Indian companies.

While offering benefits and receiving business opportunities, NRI directors also face some challenges. These are as follows:

These are some key challenges that NRI directors in Indian companies face. Further, through professional assistance and guidance, they can easily handle all these issues and enjoy their position as a company director.

Lastly, understanding the difference between an Indian resident director and an NRI director is vital for governance, compliance, and smooth corporate functioning. Additionally, especially vital for NRIs who want to stay connected to their roots while participating in the economic growth of India. Resident directors offer the necessary local presence to satisfy operational and legal requirements. In contract an NRI director brings global perspectives and strategic insights. To ensure legal compliance, strategic growth, and tax efficiency, Indian companies should balance both roles wisely.

Further, being an NRI director, if you need assistance in managing your business operations and tax planning, connect with Savetaxs. Our business experts will help you resolve all your doubts and provide complete guidance in executing your business expansion in India.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr Shaw brings 8 years of experience in auditing and taxation. He has a deep understanding of disciplinary regulations and delivers comprehensive auditing services to businesses and individuals. From financial auditing to tax planning, risk assessment, and financial reporting. Mr Shaw's expertise is impeccable.

Want to read more? Explore Blogs

_1772791127967.webp&w=828&q=75)

_1772887385012.webp&w=828&q=75)