_1773060834347.webp&w=828&q=75)

Public Company - Types, Benefits, Registration & More

Read More

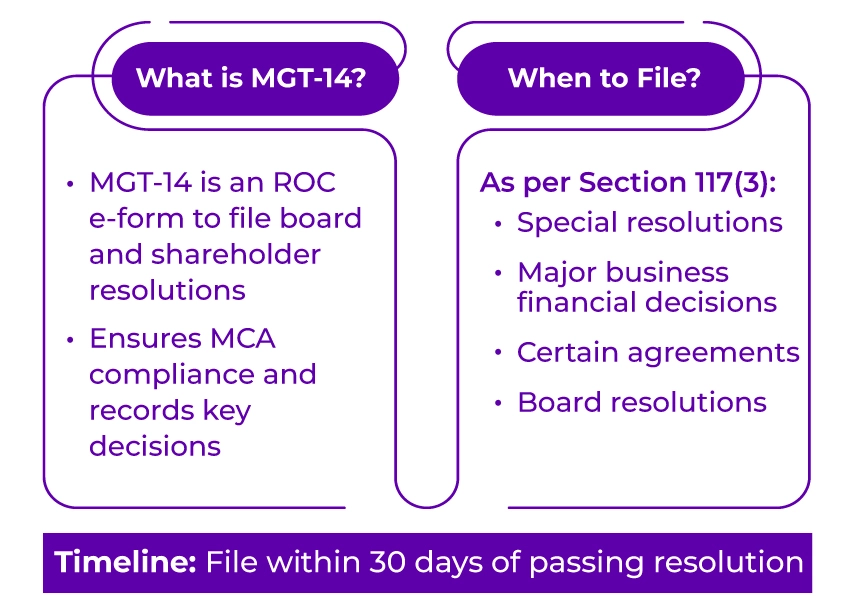

According to Section 117 of the Companies Act, 2013, the Form MGT-14 is filed with the ROC to report a specific resolution passed at a general meeting or a board meeting. It must be filed through the MCA portal within 30 days of passing the resolution or making the agreement. It is applicable to both public companies and private companies. However, for public companies, it is required only for special resolutions and specific board resolutions under Section 179(3), while for private companies, it is required for specific resolutions.

There are various types of resolutions for which filing Form MGT-14 is required. It includes ordinary resolutions, special resolutions, written resolutions, and board resolutions. The MGT-14 Form can be downloaded from the MCA portal for free. While filing the form, detailed information is required related to the company's basic details, meeting information, and resolution specifics.

The fees for filing, MGT-14, may vary based on the company's authorized share capital. For example, the fees for authorized share capital under Rs. 1,00,000 are Rs. 200. Similarly, there is an additional fee for late-filing, such as for a delay period of 16 to 30 days, a penalty of 2 times the normal fees applies. Moreover, non-compliance or late-filing can attract significant fines for both the company and every officer in default. The 30 days are calculated from the date of resolution, instead of the meeting date.

Additionally, companies must apply for condonation of the delay with the Central Government for filing that exceeds 300 days. In this guide, we will cover everything you need to know about the Form MGT-14.

The MGT-14 form is an e-form submitted by businesses to the Registrar of Companies (ROC) to report specific resolutions passed at a board meeting or general meeting. It ensures compliance by notifying the Ministry of Corporate Affairs (MCA) regarding major decisions taken by the company. It helps record changes in the company structure or operations and ensures compliance with the MCA regulations.

As specified under Section 117(3) of the Companies Act, 2013, companies must file the MGT-14 Form after passing any resolution. Some scenarios where MGT-14 filing is required include:

The applicability of Form MGT-14 varies based on the type of companies:

Public limited companies must file Form MGT-14 for:

Private limited companies must file MGT-14 for:

Under Section 179(3)(g), if private companies fulfil the following conditions, they are exempt from filing Form MGT-14 for board resolutions:

Keep in mind that these exemptions are not fixed. Hence, companies must regularly check the updates issued by the MCA to ensure compliance with the regulations. Additionally, if an NRI owns a company in India, filing MGT-14 becomes mandatory. MGT-14 becomes relevant for an NRI if they are associated with an Indian company as a director or shareholder.

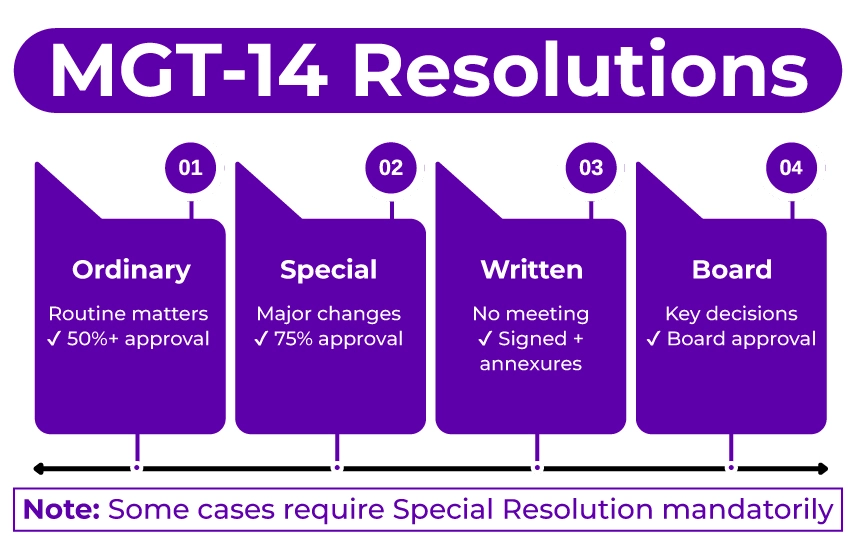

Filing Form MGT-14 is required for different types of resolutions. Each type serves a different purpose and carries certain approval thresholds. Here are the types of resolutions for MGT-14 Form filing

These resolutions are used to report routine business decisions regarding the company's day-to-day functioning. Companies usually use ordinary resolutions for decisions like:

To pass an ordinary resolution:

When a company decides to make a significant change or decision that has a long-term impact, special resolutions become mandatory. Such resolutions often have a long-term impact on the company's structure or strategy. Since the matter involved is significant, these resolutions require a higher level of agreement. As per Section 117(3)(a) of the Companies Act, companies need a special resolution when:

To pass a special resolution:

It permits the company to make formal decisions without conducting a shareholder meeting or a physical board meeting. Written resolutions can be helpful when urgent decisions are required. However, when submitting to regulatory authorities, it must be accompanied by specific annexures to ensure legal compliance:

To pass a written resolution:

As per Section 179(3) of the Companies Act, public companies need to pass board resolutions for certain important business operations. Formal board approval is required for such decisions, and it is often documented in board meetings. Here are some decisions covered under these resolutions:

Apart from these, some decisions require special resolutions, even if they are passed unanimously. It includes appointing or reappointing a managing director, changing the terms and conditions of a managing director's employment, etc. Such resolutions require careful consideration, proper documentation, and higher approval thresholds.

The table below lists the documents required for filing Form MGT-14:

|

Particulars |

Required Documents |

|---|---|

|

Mandatory Documents |

|

|

Additional Documents (if applicable) |

|

The documents must be uploaded in PDF format, and the authorized signatory must self-attest the documents.

The table below lists the comprehensive information required for filing the Form MGT-14:

|

Particulars |

Details Required |

|---|---|

|

Basic Details of the Company |

|

|

Meeting Information |

|

|

Resolution Specifics |

|

|

Supporting Form |

|

Follow the steps below to file the MGT-14 Form:

Visit the MCA website and look for the 'MCA Services' option in the main menu. Click on 'Company Forms Download' and search for 'MGT-14' in the form list. Download the latest version in PDF format for free.

Fill out all the necessary fields in the e-form MGT-14. It includes information related to the company, resolution details, and meeting specifics. After that, upload scanned copies of all the required documents in PDF format. Ensure to upload clear, readable, and properly sized documents.

Before the final submission, use the pre-scrutiny feature to identify and rectify any basic errors. After that, upload the digital signature certificate (DSC) of the authorized director or company secretary.

Use the authorized credentials to log in to the MCA portal and submit the completed MGT-14 Form online. Pay the applicable fees online using net banking, debit card, or credit card.

Upon successful submission of the form, a Service Request Number (SRN) will be issued. Use the SRN to track the form submission status and save it for future reference.

The fee for filing MCA Form MGT-14 depends on the company's authorized share capital. The table below lists the applicable fee:

|

Authorized Share Capital |

Applicable fee in INR |

|---|---|

|

Less than Rs. 1,00,000 |

200 |

|

Rs. 1,00,000 to Rs. 4,99,999 |

300 |

|

Rs. 5,00,000 to Rs. 24,99,999 |

400 |

|

Rs. 25,00,000 to Rs. 99,99,999 |

500 |

|

Rs. 1,00,00,000 or more |

600 |

The additional fee for late-filing depends on the period of delay beyond the 30-day deadline:

|

Delay Period |

Additional Fee |

|---|---|

|

Up to 15 days |

1 time normal fees |

|

16 to 30 days |

2 times the normal fees |

|

31 to 60 days |

4 times the normal fees |

|

61 to 90 days |

6 times the normal fees |

|

91 to 180 days |

10 times the normal fees |

|

181 to 270 days |

12 times the normal fees |

Ensure to file Form MGT-14 on time to avoid hefty penalties.

The Registrar of Companies (ROC) must receive the Form MGT-14 within 30 days from the date of passing the resolution or making the agreement. The 30 days are calculated from the date of resolution and not the date of the meeting.

This timeline is applicable to every company regardless of the type or resolution category. Not filing within the due date can attract additional fees as specified under the Comapnies Rules.

Under Section 117(2), non-filing or late filing of the Form MGT-14 can attract penalties:

|

Defaulting Party |

Structure of Penalty |

|---|---|

|

Company |

Initial penalty of Rs. 10,000 + Rs. 100 per day for continuous delay (Maximum Rs. 2,00,000) |

|

Officer in Default |

Initial penalty of Rs. 10,000 + Rs. 100 per day for continuous delay (Maximum Rs. 50,000) |

The penalty is calculated from the 31st day after the date of resolution. Both the company and the responsible officers will face separate penalties.

Companies are not allowed to file directly after the MGT-14 form filing exceeds 300 days. In such cases, companies must file an application for condonation of delay with the Central Government. Follow the steps below to apply for a condonation of delay due to the delay in filing Form MGT-14:

File an application with the Regional Director for the condonation of the delay through Form CG-1. Add detailed reasons behind the delay, and also include the supporting documents. Pay the amount for the penalty as specified by the Regional Director. The amount may vary based on the duration of delay and comapny's situation.

The director will review the application, and if they are satisfied with the provided reasons, a condonation order will be issued. After that, ensure to submit Form INC-28 with the ROC within the specified timeline in the condonation order. Also, attach a copy of the condonation order.

Once INC-28 is approved, file the MGT-14 form by stating the approved INC-28 SRN in the appropriate field.

Several provisions of the Companies Act, 2013, and related rules provide the legal foundation of the Form MGT-14:

Companies need to file specific resolutions and agreements with the ROC as per Section 117 of the Companies Act, 2013. It includes special resolutions and other decisions that must be reported to ensure compliance with the law.

The powers of the Board of Directors that must be used through board resolutions are listed under Section 179(3) of the Companies Act, 2013. It includes borrowing or investing funds, or approving financial statements.

According to Rule 24, companies must file the MGT-14 form within 30 days of passing specific special or board resolutions, along with a certified true copy.

While filing Form MGT-14, ensure to avoid these common mistakes to prevent rejections or penalties:

Using expired digital signatures and avoiding pre-submission checks are some common errors. Additionally, not understanding the form requirements or exemptions or filing late without paying the proper fees can also lead to penalties.

Filing unnecessary resolutions can attract penalties. Similarly, missing out on mandatory resolutions due to a misunderstanding or misclassification of exemptions for private companies.

Filing Form MGT-14 is important to maintain transparency and ensure compliance with the MCA regulations. File MGT-14 Form within 30 days of passing the resolution to avoid significant penalties and to keep your company's record clean. Additionally, if the MGT-14 form filing exceeds 300 days, applying for a condonation for the delay becomes mandatory. Since the condonation application process is complex and may have potential legal implications, seeking expert assistance from Savetaxs can help.

At Savetaxs, we are a team of experts who can provide end-to-end consultancy for the entire MGT-14 filing process. Our experts can help you with gathering the required documents, completing the process step-by-step, and even apply for condonation for the delay exceeding 300 days. You can ensure compliance and transparency with the help of experts and prevent any late-filing or non-compliance penalties. Connect with us today, and file MGT-14 Form with confidence.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr. Ritesh has 20 years of experience in taxation, accounting, business planning, organizational structuring, international trade financing, acquisitions, legal and secretarial services, MIS development, and a host of other areas. Mr Jain is a powerhouse of all things taxation.

Want to read more? Explore Blogs

_1773060689892.webp&w=828&q=75)

_1773147247383.webp&w=828&q=75)

_1773142480787_1773146465792.webp&w=828&q=75)

_1773223986036.webp&w=828&q=75)