_1766396437.webp&w=828&q=75)

Emergency Fund for NRIs – How Much to Save & Where

Read More

An index fund is an investment product that tracks the performance of a financial market index, such as the Nifty 50 or the S&P 500. NRI investors in India are particularly drawn to index funds because it offers low risk, broad market exposure, and diversified options. This is so because index funds reflect the performance of the benchmark index and may fluctuate with market movements.

Index funds are a great investment tool for investors who are relatively new to the game and looking for inexpensive options. In this blog, we will cover what index funds are, including the best index funds in India for NRIs in 2026 and more.

Index funds are a particular category of mutual funds that mimic popular market indices. These funds follow a passive investment approach that aims to closely match the returns of market indices. Index funds generally achieve this by either holding the securities within the index or a representative sample.

These funds offer investors with broad market exposure, low portfolio turnover, and lower operating expenses, making index funds a popular long-term investment opportunity for NRIs.

Index funds can benefit NRI investors in India in many ways. The following are some key advantages of an Indian fund and reasons why NRIs invest in it.

As aforementioned, in index funds, fund managers generally follow a passive investment strategy. Therefore, they do not select stocks individually; instead, they replicate the particular index. The passive strategy helps minimize costs, ultimately lowering the overall expense ratio, making the index fund a cost-efficient investment product for NRI investors.

NRI investors who choose to invest in index funds also enjoy the benefit of diversification. The passive management by the fund managers makes this investment product unique. The manager simply replicates the structure of the selected index. Index funds copy or mimic a selected index and invest in a range of different stocks that make up that index. This broad market exposure helps investors spread risk across different industries, companies, and sectors.

An index fund is prepared to specifically replicate the performance of a selected underlying index that has shown consistent growth over the years. Whereas individual stocks are unpredictable and change quickly. In a nutshell, index funds offer consistent performance with long-term growth, allowing investors to participate in the market's overall upward trend.

When it comes to investments, portfolio diversification is the best advice. Many investors agree that investing in a single stock is never a wise idea, and an index fund tracks an index; hence, investing across the industries and companies in the specific index appeals to NRI investors. Diversification minimizes risk, as the poor performance of one company does not affect the index fund's overall performance.

Index funds have a low turnover, meaning few trades are placed in a year. This generally happens because index funds are passively managed. The lower turnover of index funds results in fewer capital gains distributed to investors. Additionally, many index funds follow a buy-and-hold approach, which ultimately enhances tax efficiency.

We help NRIs file their ITR in India hassle-free with 24/7 expert support.

Selecting the right index funds as an NRI is not a cakewalk. This generally requires a strategic evaluation of the fund's efficiency, expense ratio, and consistency. The following are some of the best Indian index funds for NRIs in 2026.

| Name Of The Fund | AUM (Rs) Cr | 1 Year Return (%) | 3 Year CAGR (%) | Expense Ratio (%) |

|---|---|---|---|---|

| UTI Nifty 50 Index Fund | ₹24,433.24 Cr | +5.38% | +11.20% | 0.20 |

| HDFC Index Fund - Nifty 50 Plan | ₹20,436.59 Cr | +5.33% | +11.16% | 0.20 |

| ICICI Prudential Nifty Next 50 Index Fund | ₹7,604.43 Cr | +9.75% | +20.70% | 0.31 |

| SBI Nifty Index Fund | ₹11,216.86 Cr | +5.30% | +11.71% | 0.19 |

| Nippon India Index Fund - Sensex Plan | ₹849.49 Cr | +3.15% | +9.40% | 0.20 |

The aforementioned funds in the table are widely recognized as the Best Index Funds for RIs in India due to their long-term track record, cost efficiency, and liquidity.

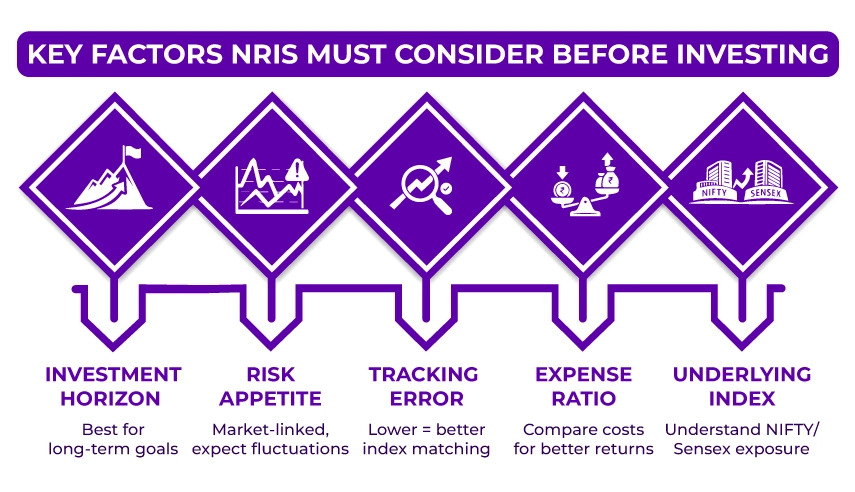

The following factors are important for NRI investors to consider before investing in Indian index funds, ensuring their investment aligns with their long-term financial goals and risk appetite.

The following is a simple step-by-step method on how NRIs can invest in index funds:

NRI investors, please note that many platforms in India allow investments starting at 500 Rs per month.

The taxation of index funds depends on the investment's holding period. Now that most of the index funds invest primarily in equities, they are typically taxed as equity mutual funds.

NRI investors must consider the tax implications and the holding period of the funds while planning their investment.

Our experts provide end-to-end consultation on NRI investment matters.

NRIs who believe that the Indian investment market will outperform in the future must invest in index funds. However, please ensure that, like mutual funds, index funds also come with different levels of risk; hence, do your research thoroughly and consult an NRI investment advisor before planning your investment strategy in the Indian market.

When it comes to an NRI investment advisor, Savetaxs is the name to trust. Our experts provide end-to-end consulting to NRI investors on managing their financial portfolios, tax compliance, and cross-border investments. The experts ensure that FEMA, RBI, and DTAA regulations are strictly adhered to. Furthermore, the experts provide consultation on investments in Indian index funds, NRE/NRO account management, investment portfolio management, tax optimization, regulatory compliance, and more.

Connect with us as we serve our clients 24/7 across all time zones.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr. Ritesh has 20 years of experience in taxation, accounting, business planning, organizational structuring, international trade financing, acquisitions, legal and secretarial services, MIS development, and a host of other areas. Mr Jain is a powerhouse of all things taxation.

Want to read more? Explore Blogs

_1766492717.png&w=828&q=75)

_1766561286.webp&w=828&q=75)

_1766561266.webp&w=828&q=75)