What is the Difference Between Domestic vs Global vs International Funds?

Read More

_1773319924819.webp&w=3840&q=75)

Systematic Investment Plans (SIPs) have become one of the most popular ways for resident Indians and NRIs to invest in mutual funds in India. As an investor, you might wonder whether SIP is tax-free or not. The clear answer to it is no, as they attract tax on dividends and capital gains. However, compared to other investment tools like fixed deposits, with a proper investment plan, SIPs are highly tax-efficient.

Further, to help you out, this blog covers all things associated with SIP taxation- from tax rates, exemptionsm deduction, and benefits to strategies that help in saving taxes. So read on and gather all the information.

Systematic Investment Plan or SIP can be defined as an investment plan where an invest contribute a fixed amount regularly, quarterly, or monthly into a mutual fund scheme of their choice. Considering this, unlike other investments, SIP instead of making large lump sum payments. allow you to take a disciplined method and systematically invest your savings.

Additionally, it also offers you the flexibility to invest in an SIP monthly, yearly, semi-annually, or quarterly that aligns with your income and financial goals.

This was all about SIPs. Now moving ahead, let's know the benefits of investing in SIPs.

The following benefits are offered by SIP to its investors:

These are some of the key benefits SIP offers to its investors. Moving further, let's know about the different types of funds included in SIP.

The tax treatment of SIP depends on the mutual fund type you invested in and the holding period. Considering this, based on whether they are equity-oriented or debt-oriented mutual funds, they are taxed at different rates.

As per SEBI, a fund can be stated as equity-oriented if it has at least 65% of its assets invested in equity-related instruments or stocks. So hybrid funds, as well as pure equity funds, with a minimum of 65% if assets allocated to equities for taxation purposes, are stated as equity-oriented funds. For instance, hybrid funds such as equity savings schemes that only invest 30 to 40% of their assets in stocks. However, because of their arbitrage allocation, they are taxed as equity-oriented funds.

Debt-oriented funds are just the opposite of equity-oriented funds. Considering this, if less than 65% if a mutual fund's assets are invested in equity, they are called a debt-oriented fund. It includes pure debt schemes like liquid funds and debt-oriented hybrid funds.

This was all about the mutual fund types. Moving ahead, let's know the type of income earned in SIPs.

There are two ways in SIPs to income, and each is taxed differently. These are as follows:

When the units of the funds are redeemed, or on a stock exchange, you sell them or close the mutual fund schemes, the profit generated from them is called capital gains. In simple words, it can be defined as the difference between the purchase price and the selling price of the mutual funds.

If you have invested in SIP through the IDCW (Income Distribution cum Capital Withdrawal) option, the income you regularly earn is taxed like dividends. Dividends paid on both debt and equity mutual funds are taxed according to the income tax slab rate of the investors. In cases other than mutual funds, the investor does not have any income source, and a 10% mandatory TDS is deducted from the total dividend income. However, if the dividend distribution is INR 5,000 or less, no TDS is deducted.

These are the types of income received by investors in SIPs. Moving further, let's know another key factor, i.e., the holding period that decides the SIP taxation.

As its name states, it refers to how long a mutual fund investment has been held before being redeemed or sold. According to the holding period, capital gains are classified into short-term capital gains (STCG) or long-term capital gains (LTCG). Based on the holding periods, both equity and debt mutual fund SIPs have different tax rules.

Here, you need to consider an important point that, for a lump sum investment, calculating the holding periods is quite simple, but in the case of SIP, it becomes quite difficult. It is because every SIP installment is stated as a separate investment. Therefore, for tax calculation purpose it has its own holding period.

This was all about holding period rules for SIP taxation. Moving forward, let's know how SIP taxation works.

The tax implications for SIP depend on the mutual fund type, the duration you hold the funds, and the type of income earned. Considering this, whether the mutual funds are equity or debt-oriented, their holding period was short-term or long-term. Additionally, the income generated from it was capital gains or dividend income.

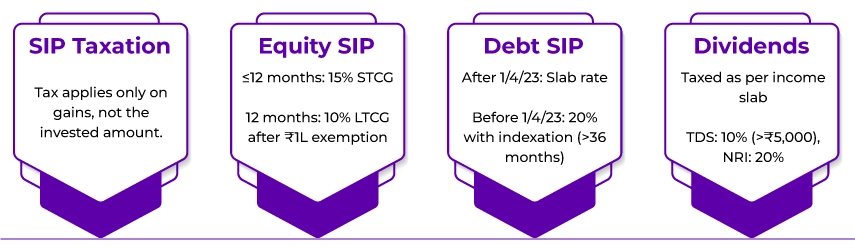

Apart from this, the point to remember is that in SIP, the invested amount is not taxed, but the gains on it are taxed. Each mutual fund type has specific rules for capital gains tax, exemptions, and lock-in periods.

This was all about how SIP taxation works. Let's know more about the taxation of capital gains from SIPs in more detail.

Here is how capital gain on equity-oriented SIPs is taxed:

If the equity funds are held for 1 year or less, and after that, they are redeemed or sold, they are classified as short-term capital gains. Section 111A of the Income Tax Act, 1961, defines how STCG tax is imposed on equity funds. According to Section 111A of the Income Tax Act, short-term capital gains on equity mutual funds are taxed at 20%.

If the equity funds are held for more than 1 year and after that they are sold or redeemed, they are classified as long-term capital gain. According to section 112A of the Income Tax Act, 1961, LTCGs are taxed at 12.5%, with the first INR 1,25,000 tax exempt in that financial year. For instance, if you earn INR 3,00,000 LTCG from an equity fund, 12.5% tax will be imposed only on INR 1,75,000.

Further, these tax rates during the Union Budget 2024 were announced by the Indian government. Considering this, if you hold equity fund SIPs before July 23, 2024, the old SIP tax rate, i.e., STCG- 15% and LTCG- 10%, would apply to you.

So, here is how equity-oriented SIPs are taxed. Moving further, now let's know about the capital gains tax on debt-oriented SIPs.

In recent years, with major changes stated during the Union Budget 2023 and 2024, debt fund taxation has gone through significant changes. Considering this, if you have invested in these funds after April 1, 2024, debt capital gains taxation is quite easy. It is because, irrespective of the holding period, tax is imposed as per your income tax slab rate without any indexation benefits. However, if you have invested before April 1, 2023, taxation becomes quite difficult.

Here is investments sold before July 23, 2024 were taxed:

Here, a new rule that revised the holding period was introduced by the government:

Here, the 24-month holding period is for unlisted securities. For listed securities, the holding period is 12-months.

This is how debt-oriented SIPs are taxed. Moving ahead, let's know the Tax Deducted at Source (TDS) imposed on SIPs.

Resident Indians are not liable to pay TDS on capital gains. However, NRIs are subject to paying TDS on capital gains received from SIP investments.

Mutual funds with IDCW option at regular intervals distribute earnings in the form of dividends to investors. Considering this, if you have invested in any such scheme, you are liable to pay tax on your SIP returns. Before 2020, the government imposed a dividend distribution tax under which tax was deducted by the mutual fund houses.

However, it is now abolished, and investors are now accountable to deduct tax on income from IDCW funds. Considering this, income from IDCW funds is now added to the total income of investors and is taxed under the head of "income from other sources" as per their tax slab rate.

Income generated from IDCW funds is subject to TDS. Considering this, for resident investors, if the dividend income is more than INR 5,000 attracts 10% TDS. Considering this, before crediting the income to your account, 10% TDS is deducted by the mutual fund houses. For NRIs, the TDS rate is higher, i.e., 20%. However, through DTAA, they can lower this TDS rate.

This was all about TDS deduction on SIPs. Moving ahead, let's know about how SIP helps in saving taxes.

Here is how investing in SIPs helps you save taxes

Equity Linked Savings Scheme is one of the types of mutual funds popular for its tax efficiency. Under section 80C, ELSS investors are allowed to deduct up to INR 1,05,000 from their taxable income. This is why they are called tax-saving mutual funds. Therefore, an investor with 30% slab rate by investing in ELSS can save up to INR 46,800 per year.

Further, among the 80C tax-free investments in India, like SSCS, PPF, and NPS funds, ELSS funds have 3year lock-in period, which is the shortest among other investments. Additionally, as these funds heavily invest in equities, investing in an ELSS SIP plan for five years or more can provide you with better returns.

Funds with the growth option reinvest their returns, which results in a high NAV. Further, as these funds do not pay any dividend income generated from these funds is taxed as capital gains.

In contrast to this, IDCW funds distribute regular income to their investors, which further results in low NAV. Additionally, on them, capital gains taxes are imposed upon redemption and on the income earned as dividend taxed at the applicable slab rate. For investors with higher tax brackets, this tax liability could be significant.

Considering this, if you do not want a regular income and want to invest in long-term growth funds is a good option with favourable taxation.

Due to the lower tax rate on long-term investments, investing in equity funds provides investors with better returns.

You can exempt up to INR 1,25,000 tax on LTCG earned from equity investments in a financial year. You can take advantage of this tax exemption by making a systematic withdrawal and minimizing your tax obligation.

If you are confused about investing in SIP funds or facing issues in choosing the right mutual fund, consider taking the help of a professional. With an expert by your side, you will not only save your money but also effectively work towards achieving your financial goals through proper investment planning.

These are some of the tax planning strategies with SIPs for investors. Moving forward, let's know about the SIP tax benefits.

Investing in ELSS SIP plans helps you take advantage of a tax deduction of up to INR 1,05,000 per financial year. Additionally, as these funds have a lock-in period of three years, upon redemption, only LTCG is imposed on them. Considering this, with ELSS SIPs, you can enjoy reduced tax rates and benefits from LTCG tax exemption. Additionally, with a smart withdrawal strategy, you can make your in the long run more effective.

This was all about SIP tax benefits. Now, moving further, let's know when is the right time to start investing in SIP.

Ideally, to start investing in SIP every time is right. It is because SIP gets the benefit from compounding interest, which was once called the "eighth wonder of the world" by Einstein. When you reinvest your returns, they earn their own profits, which further create an exponential effect. Confused, let's better understand this with an example.

Consider that with a 12% expected rate of return, in an equity fund, you invested INR 5,000 per month. In 15 years, the value of your investment from INR 9,00,000 increased to INR 25,00,000. Now, suppose you stay invested for five more years, i.e., 20 years in total. The value of your INR 12,00,000 investment grows to INR 50,00,000 approx. Here you can see that the longer you invest in SIP, the more your returns will increase.

Another reason why you should not waste time and start investing in SIP is rupee cost averaging. With lump sum investments, you need to be careful about the right time to invest. However, in the case of SIP, this is not the case. With the rupee cost-averaging SIP, make sure you purchase more units when prices are low and fewer units when prices are high. It helps to average out the price of your investment.

Even tax-wise, early planning can be beneficial, as you won't be running for last-minute investments in tax saving SIP to save taxes. Additionally, at the end of the financial year, rushing to tax-saving instruments like ELSS may help you in saving your some tax on your SIP returns. However, without conducting proper research, investing in them can lead to choices that may not match your financial goals and risk appetite.

Connect Savetaxs and choose the right investment plan that aligns with your financial goals and risk appetite.

Lastly, although SIPs are not tax-free, they do offer tax efficiency. Considering this, in SIPs, the principal amount is not taxed. However, capital gains received on these investments are taxed. Further, under section 80C, by investing in ELSS SIPs, you can get the tax benefits.

If you are facing issues in choosing the right investment, connect with Savetaxs. We have a team of financial experts who can assist in selecting the correct SIPs that align with your wealth-building and tax-saving goals.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr. Ritesh has 20 years of experience in taxation, accounting, business planning, organizational structuring, international trade financing, acquisitions, legal and secretarial services, MIS development, and a host of other areas. Mr Jain is a powerhouse of all things taxation.

Want to read more? Explore Blogs