_1772801423285.webp&w=828&q=75)

Difference Between Joint Property vs Sole Property Ownership for NRIs

Read More

_1773233466269.png&w=3840&q=75)

Family trusts are important for NRIs as it offers a structured way to hold and manage assets in India, especially if you hold assets exceeding Rs. 10 crore. It helps hold the assets under defined rules to ensure clarity and control. A trust also avoids probate and keeps the family's financial matters confidential. You should consider creating a family trust based on your objectives and wealth-size. Family trusts follow a strong structure, where the trustee manages the assets, and the beneficiaries enjoy the benefits.

Trusts also offer a great solution to inheritance planning and wealth management for NRIs. It stays active during your lifetime and can last for decades or even several centuries. The trust is liable to file returns annually and pay tax on any income generated in India. They must report the income related to the trust in their country of residence. Additionally, a trust must be created with a clear objective and defined goals. NRIs must appoint a reliable trustee as they hold significant powers, and they must follow the residency and reporting rules to avoid penalties. Keep reading this blog to know more about why family trusts are important for NRIs.

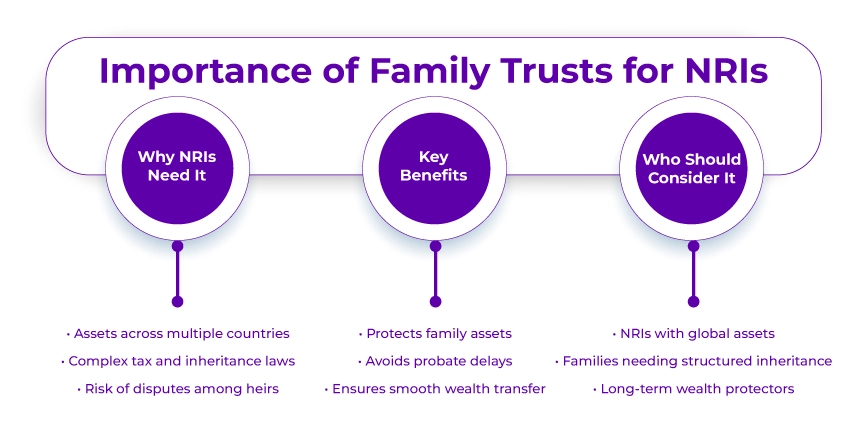

NRI wealth planning is often more complicated for NRIs as compared to resident families. Their assets may be spread across multiple countries, like a property in India, investments abroad, and a business overseas. foreign bank accounts, etc. If you don't plan everything with a structure, this complexity will lead to legal confusion, tax inefficiency, and disputes among the heirs. This is when family trusts play an important role and become highly relevant.

A family trust offers a structured way to hold and manage assets for the benefit of chosen family members. It ensures clarity and control by helping to hold the assets under defined rules rather than transferring them directly to the heirs. It is important for NRIs because various countries may have different laws regarding inheritance, taxes, and reporting.

Under certain jurisdictions, probate proceedings can be time-consuming. A trust structure usually avoids probate and ensures privacy by keeping the family's financial matters confidential. This choice can be invaluable for families having significant assets or business interests.

Family trusts also help NRIs in creating stability across generations. You get the ease to define how the wealth will be distributed, managed, or preserved after your demise.

Not everyone needs to set up a family trust. However, you can consider setting up a family trust for two main reasons: your objectives and your wealth size. Here is why:

Under some circumstances, a family trust may become very important, such as:

Size of Your Wealth

A family trust becomes mandatory if you hold assets exceeding Rs. 10 crore in India. As an NRI, such significant wealth protection for NRIs remotely can be complicated. These assets can even lead to legal issues and disputes if proper planning is not done. Creating a family trust can easy managing everything and offer stability as well.

A family trust has an easy yet strong structure:

For example, suppose you transfer your house, investments, or business shares into the trust. The trustees will be responsible for managing the assets, and the beneficiaries will enjoy the perks, like rental income or dividends. However, the principal amount will remain safe and protected.

When talking about trust vs will for NRIs, there are a lot of differences. A will takes effect only after your demise and often involves complicated legal procedures. On the other hand, a trust stays active during your lifetime, which helps you look after how your wealth is being managed right now. Here's why a family trust is better than a will for NRIs:

It serves as financial security for your family's future, which is managed professionally with clear and long-term rules.

Creating a trust involves the following tax obligations that NRIs must consider to ensure compliance:

Here are some common mistakes that an NRI must avoid while creating a family trust:

Get CA-approved NRI investment strategies tailored to your financial goals.

NRI estate planning requires considering various factors, including cross-border laws, religious succession rules, and tax obligations. A trust offers various benefits to NRIs as compared to a will. NRIs having significant assets, global financial responsibilities, and complicated family needs, a trust can be a practical tool for them. A trust not only helps with wealth management for NRIs but also serves as a gift of security, clarity, and stability for your upcoming generation.

Additionally, to ensure your planning for a private family trust in India works smoothly across borders, consider seeking assistance from an expert at Savetaxs. Trusted by NRIs worldwide, Savetaxs has a team of experts who can help you take the right steps and create an effective family trust based on your assets and financial goals. They will guide you in structuring the trust according to your requirements and review everything carefully to avoid potential issues.

Reach out to us now and get personalized guidance for NRI estate planning, inheritance planning, and tax planning strategies.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr. Ritesh has 20 years of experience in taxation, accounting, business planning, organizational structuring, international trade financing, acquisitions, legal and secretarial services, MIS development, and a host of other areas. Mr Jain is a powerhouse of all things taxation.

Want to read more? Explore Blogs

_1772886992475.webp&w=828&q=75)

_1773319924819.webp&w=828&q=75)

_1773751977541.png&w=828&q=75)