A repatriable demat account is through which NRIs can invest in Indian capital and equity markets and easily repatriate the funds generated from these investments overseas. This account serves both as a transactional and regulatory tool under the foreign exchange and securities laws of India.

However, to ensure compliance and optimize financial planning, it is vital to understand how a repatriable demat account operates. To help you out, this blog consists of all the information associated with an NRI repatriable account, from its meaning to how to open this account. So read on and solve all your doubts about.

Key Takeaways

- A repatriable demat account lets NRIs invest in India and transfer the principal, profits, and dividends back abroad freely.

- A repatriable demat account should be linked to an NRE bank account.

- It allows unrestricted transfer of investment proceeds, i.e., capital and earnings, out of India.

- A repatriable demat account is governed by FEMA and RBI guidelines, certifying compliance.

- Though interest is tax-free, investment returns and capital gains are taxable in India according to Indian tax laws.

Repatriable Demat Account for NRIs: Meaning and Purpose

A repatriable demat account allows NRIs to hold and trade Indian securities while allowing them to transfer their principal amount and investment income freely to their resident country. Further, let's know the key features of the NRI repatriable account:

- It should be linked to a Non-Resident External (NRE) savings account.

- You can send both capital and returns from investment without any restrictions abroad.

- For overseas remittance, this account is governed by RBI and FEMA guidelines.

- In repatriable demat accounts, the funds should be obtained from foreign earnings or NRE bank account deposits.

Additionally, this account is suitable for NRIs who want complete flexibility to move their investment earnings between India and overseas.

For instance, if you are working in the UK and via your NRE-linked demat account, invest INR 4,00,000 in Indian stocks. In this scenario, without any special approvals, you can transfer the principal or profits back anytime to your US bank account.

This was all about repatriable demat accounts for NRIs. Moving ahead, let's know the key features of this account for NRIs.

Key Features of NRI Repatriable Demat Account

Here are some of the key features of an NRI repatriable demat account:

- An NRI demat repatriable account is opened by NRIs who want to transfer funds from abroad and use them to purchase shares and other securities in the Indian market. Additionally, through a demat account, hold them in electronic custody.

- This account should only be linked to your NRE bank account, as it is a repatriable bank account. Considering this, you cannot link this account with the NRO account as it is a resident account, and with this account, you cannot perform the repatriation process fully.

- Since the NRI repatriable demat account is linked to the NRE bank account, it is also called an NRE demat account or a repatriable demat account.

- All earnings from the dividend, the sale of securities, and capital gains can be transferred fully without any restrictions.

- Additionally, if you want to purchase shares for repatriation and non-repatriation, then you need to open two separate demat accounts. Considering this, you cannot mix the NRE and the NRO demat accounts. Also, both accounts should be kept distinct from one another.

- Apart from this, the NRE demat account has two sub-accounts, i.e., NRE PIS account and NRE Non-PIS account. The NRE PIS account is used for trading in shares listed on the BSE and the NSE. In contrast, the NRE Non-PIS account is used to invest in ETFs, mutual funds, IPOs, and the sale of any shares gets as splits or bonuses.

- For direct stock investment, it is vital to take PIS permission. However, it is not required for ETFs and mutual funds. Additionally, NRIs cannot engage in short selling or intraday trading.

These were the key features of the repatriable demat account for NRI. Moving further, let's know how NRIs can invest through these accounts.

What NRIs Can Invest in Through a Repatriable Demat Account?

Here is what NRIs can generally invest in through a repartiable demat account:

- NRE FDs: Non-resident external fixed deposits provide you with the freedom to move your foreign earnings. In this, you need to keep your invested money for a minimum of one year. Additionally, early withdrawal from these investments can result in penalties. Also, the interest earned from these is free from all taxes in India, which makes it an attractive option for tax planning.

- FCNR Deposits: Foreign Currency Non-Resident deposits keep your money safe from the risk of currency by holding it in GBP, USD, or EUR. Additionally, compared to NRE FDs, these have a better interest rate and need to invest it for 1 to 5 years. Also, you can transfer investments and interest amounts overseas without any restrictions.

- Mutual Funds via NRE Account: The RBI permits NRIs to invest in mutual funds and allows fund transfer overseas. This means if you purchase funds through NRE accounts, you can move both your profits and investment back home. Further, with equity-focused mutual funds, this works well.

- Listed Equities: The Portfolio Investment Scheme (PIS) with full transfer benefits lets you purchase shares on Indian stock exchanges. Considering this, NRIs can individually keep up to 5% shares of a company. Additionally, their total ownership is limited to 10%. However, through resolution, companies can increase the NRI ownership to 24%.

- Property Sale Proceeds (Conditions Applied): With certain limits, you can transfer the money you get from the property sale. Further, the transfer amount cannot be more than what you paid originally using foreign money through banking channels.

These are the investments that NRIs can make through an NRI repatriable demat account. Moving ahead, let's know the taxation and repatriation rules for NRIs in a repatriable demat account.

Taxation and Repatriation Rules for NRIs

Many NRIs think that the NRE account provides them with tax-free benefits. However, it is not so. Considering this, even in a repatriable account:

- Profit from selling shares, i.e., capital gains, is taxable in India based on the holding period.

- Dividends are also taxable.

- In cases of NRIs, more TDS is deducted.

So, from the above information, you can say that repatriable demat accounts provide transfer not tax-free benefits. Further, let's know about the repatriation rules for an NRI repatriable demat account.

Repatriation Rules (Sending Money Overseas)

Generally, from a repatriable demat account, NRIs can send overseas:

- Investment amount

- Profit after tax, capital gains

- Divided after TDS deduction

Considering this, the money from your repatriable demat account is first credited to your NRE account, and then it is remitted abroad. Additionally, you do not need RBI approval to transfer your money from this account to your overseas bank account.

So, this was all about taxation and repatriation rules for NRIs having a repatriable demat account. Moving further, let's know how to open this demat account.

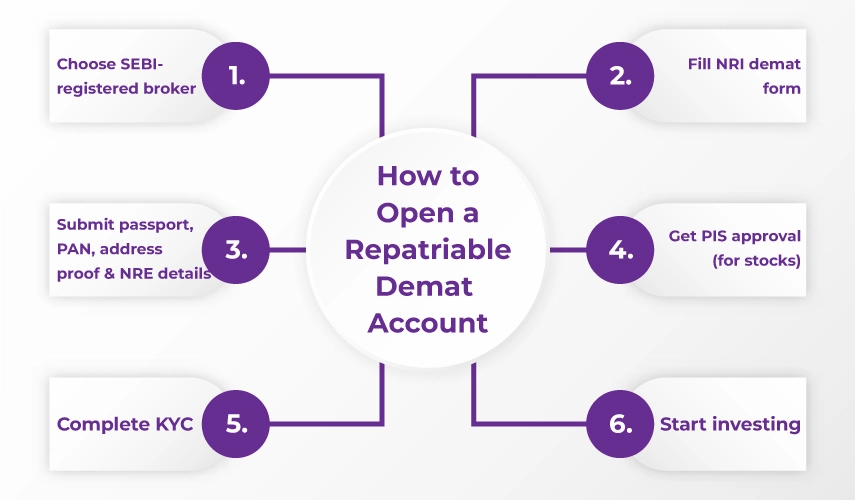

How to Open a Repatriable Demat Account?

Here is how you can open a repatriable demat account:

- Step 1: Select a SEBI-registered Depository Participant (DP) or stock broker.

- Step 2: Fill out the Demat account opening form available for NRIs.

- Step 3: Submit the required documents

- Copy of passport

- Overseas address proof (rental agreement, utility bill, or bank statement)

- PAN Card (for stock market transaction it is a mandatory document)

- NRE bank account details

- FEMA declaration form

- Step 4: For stock investment, take the PIS permission.

- To invest in the stock market of India, from the RBI, you need to obtain Portfolio Investment Scheme (PIS) approval.

- In the case of mutual fund investment and ETFs, it is not mandatory to take PIS approval.

- Step 5: Complete verification. While some brokers can accept it through a video call, others may ask for an in-person visit.

- Step 6: Once your application is verified by the broker, your repatriable demat account will be activated. Further, you can start trading in Indian securities.

This is how, by considering the above steps, you can simply open an NRI repatriable demat account.

Safeguard Your Financial Future in India

Connect with Savetaxs and with our expert financial planning services, secure your financial future today.

Final Thoughts

Lastly, a repartiable demat account is a good option for NRIs who want to invest in the Indian stock markets while ensuring easy transfer of funds overseas. The best feature of this account is that you can transfer funds from the sale of the dividends or assets without any limitations. Additionally, the interest on these investments is also tax-exempt in India.

Furthermore, if you need assistance with your investments and opening a bank account in India, connect with Savetaxs. Our financial experts will provide you with complete guidance and help you in resolving all your queries.

_1766396437.webp&w=828&q=75)

_1773751977541.png&w=3840&q=75)

_1766492717.png&w=828&q=75)

_1766561286.webp&w=828&q=75)

_1766561266.webp&w=828&q=75)