_1771327215415.webp&w=828&q=75)

What is the Difference Between Inheritance and Succession for NRIs?

Read More

Gilt funds are mutual funds that invest in securities issued by the central and state governments. Due to its sovereign backing, these funds are stated as one of the safest debt instruments in India. Gilt funds aim to provide stability, safety, and reasonable returns to the investors. Further, NRIs can invest index based Gilt funds or actively managed Gilt funds.

Want to know more about Gilt funds for NRIs? Read the blog and know everything about it, from its meaning, benefits, to who should invest in it, and so on.

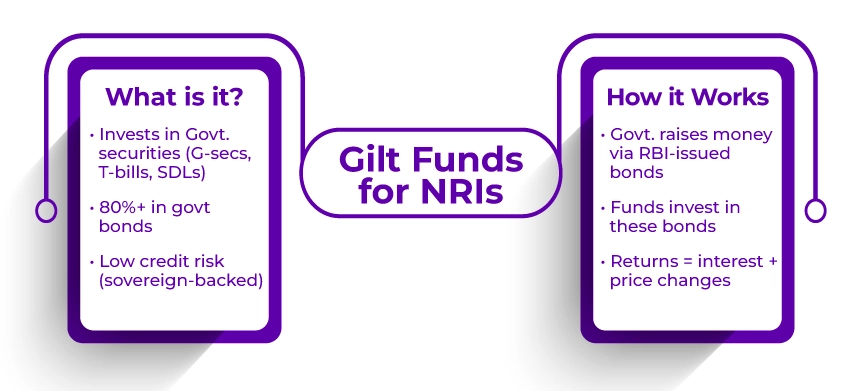

The term "gilt" comes from the word "gilt-edged," which refers to high-quality bonds issued by the Indian government that virtually carry no default risk. In simple words, these are debt mutual funds that primarily invest in government-backed securities. These funds generally include government of India securities (G-secs), Treasury Bills (T-bills), and State Development Loans (SDLs). These are all backed by the sovereign.

Additionally, the Gilt mutual fund allocates a minimum of 80% of its assets in government securities. The investment horizon of these funds ranges from medium to long-term maturities (three to twenty years).

Further, as these investments are backed by the government of India, unlike other investments in terms of debt, these are considered to have low risk. However, such funds are not unaffected by the interest rate fluctuations, which impact returns given the market conditions. These funds are somewhat stated as a traditional option for investment and are often involved in government mutual funds, providing low-risk investors.

This was all about Gilt mutual funds. Moving ahead, let's know the benefits of investing in these funds.

By investing in a Gilt fund, as an NRI, you can get the following benefits:

These are some of the key benefits that NRIs get while investing in Gilt funds. Moving further, let's know who should invest in these funds.

Gilt funds are suitable investment options for:

This was all about who should invest in Gilt funds. Moving forward, let's know how to invest in these funds.

The Reserve Bank of India (RBI) is considered the banker of banks and the apex bank of India. Considering this, when the state or central government needs funds, it approaches the RBI. After borrowing from other financial entities such as banks and insurance companies, the RBI provides funds to the government.

Further, in exchange for the loan,G-secs are issued through auctions and are purchased by gilt funds in the market. Upon maturity, the government securities are redeemed at maturity, and the principal amount is paid back to the fund. For investors, the funds are a perfect combination of reasonable returns and low risk. However, the performance of these funds is highly dependent on the movement of interest rates. So, gilt funds generally perform better during falling interest rate cycles, though timing such movements is difficult.

Moreover, the mutual funds that invest in these securities are known as Gilt mutual funds. In this, you can invest even a small amount and get exposure to well-diversified G-secs.

So, here is how Gilt funds work. Moving ahead, let's know how these funds are taxed.

Gilt mutual funds are a type of debt mutual funds and they are taxed according to it. Due to updates in the Union Budgets of 2023 and 2024, these funds faced changes in their tax treatment. To provide you with an idea, here is an overview of the present tax implications.

These tax rules apply to investments made before April 1, 2023

These tax rules apply to investments made after April 1, 2023

Impact on investments made before April 1, 2023

This was all about how Gilt funds are taxed in India. Moving further, let's know things to consider as an investor while investing in these funds.

Here are the following things that you need to consider while investing in Gilt funds:

These are some of the things that NRIs need to consider when investing in Gilt funds.

Connect with Savetaxs and plan better with expert assistance while minimizing your tax obligations.

Lastly, being a type of debt mutual fund, Gilt funds for NRIs are a suitable option for those seeking low-risk investments that provide stable income. However, before investing in these funds, it is vital to understand their meaning and how they work. It helps in making informed investment decisions. Additionally, also helps you in building a diversified investment portfolio.

Further, if you need any assistance while investing in these funds, connect with Savetaxs. Our financial experts will provide you with complete assistance from start to end. With them by your side, you will be able to make a correct investment decision as per your financial goals, risk tolerance, and time horizon.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr. Ritesh has 20 years of experience in taxation, accounting, business planning, organizational structuring, international trade financing, acquisitions, legal and secretarial services, MIS development, and a host of other areas. Mr Jain is a powerhouse of all things taxation.

Want to read more? Explore Blogs

_1771419038394.webp&w=828&q=75)