Legal Checklist For Starting A Business In India As An NRI

Read More

External Commercial Borrowings (ECBs) are loans raised by eligible Indian entities from recognized non-resident lenders. These are raised for business purposes only, in the form of loans, bonds, or other financial instruments, denominated in either Indian or foreign currency. The proceeds from ECBs can be used to fund a variety of purposes, including expansion of business and purchase of assets. It is regulated by the Reserve Bank of India (RBI), which sets limits on the ECBs that a company can access, along with the purpose for which they can be used.

There are two main routes to ECBs: the automatic route, which requires no prior RBI approval, and the approval route, which requires RBI approval. ECBs can be of various types based on the currency structure, loan features, and financial arrangements. It includes foreign-currency-denominated ECBs, rupee-denominated ECBs, convertible ECBs, and trade credit ECBs. Although very beneficial, ECBs can also carry some risks, such as currency risk, hedging cost, economic risk, and reputation risk.

Moreover, as per RBI amendments, LLPs are also permitted to raise ECBs, subject to prescribed conditions and restrictions. Keep reading further to know more about external commercial borrowings (ECBs).

External Commercial Borrowings (ECBs) are funds borrowed by Indian companies from foreign sources for business purposes. It can be obtained from various non-resident sources, such as foreign banks, international financial institutions, and foreign subsidiaries of Indian companies. ECBs can be raised in the form of loans, bonds, or other financial instruments in both Indian currency and foreign currency. The funds can be used for various purposes, including business expansion, acquiring assets, and repaying existing debts.

The Reserve Bank of India (RBI) regulates ECBs under the Foreign Exchange Management Act (FEMA), 1999. The RBI states the purpose for which ECBs can be used and sets limits on the amount of ECBs that Indian companies are eligible to obtain. ECBs must comply with some criteria, including minimum maturity period, permitted and non-permitted end-uses, etc. Only entities specifically permitted under RBI ECB guidelines, such as companies and eligible LLPs, can raise ECBs.

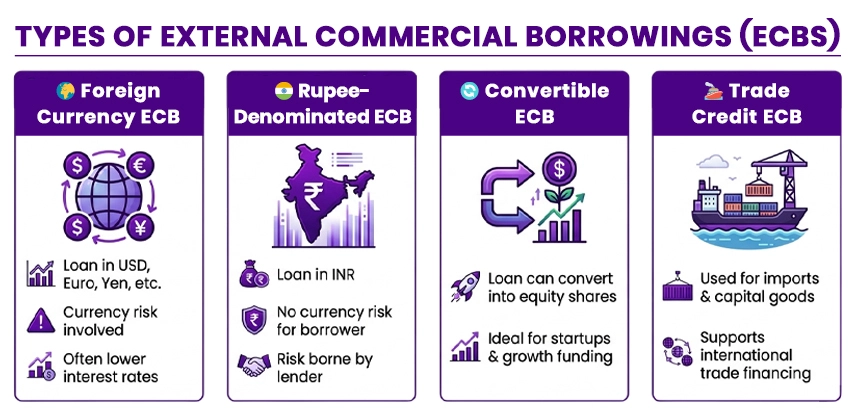

There are several types of external commercial borrowings (ECBs) based on the structure of currency, features of the loan, and financial arrangements. Businesses must choose the appropriate type based on their funding needs and financial goals. Here are the types of external commercial borrowings (ECBs):

Foreign currency-denominated ECBs refer to loans borrowed in international currencies, like the euro, US dollars, or Japanese Yen. The borrower is liable to repay the loan in the same currency, including both the principal and interest amount.

Although these loans expose companies to the risk of currency fluctuations, they can sometimes offer lower interest rates. The repayment burden will increase if the domestic currency depreciates.

The loan is provided in Indian currency in rupee-denominated ECBs, even though the lender is outside India. Since the repayment occurs in rupees, this arrangement benefits the borrower as it reduces currency risk. The overseas lender usually bears the currency risk in this case.

Convertible ECBs allow lenders to convert the outstanding loan into equity shares of the borrowing company. This arrangement is sometimes used in financing startups or venture investment structures. It allows investors to take part in the company's future growth in case the business performs well.

This arrangement is used to finance import transactions or acquire capital goods from overseas suppliers. It helps companies to handle international trade transactions and finance the purchase of equipment.

Each type of ECB carries different financial implications and regulatory requirements. So, you must ensure to choose the relevant type based on your entity's funding needs.

File NRI taxes with expert guidance and stay compliant

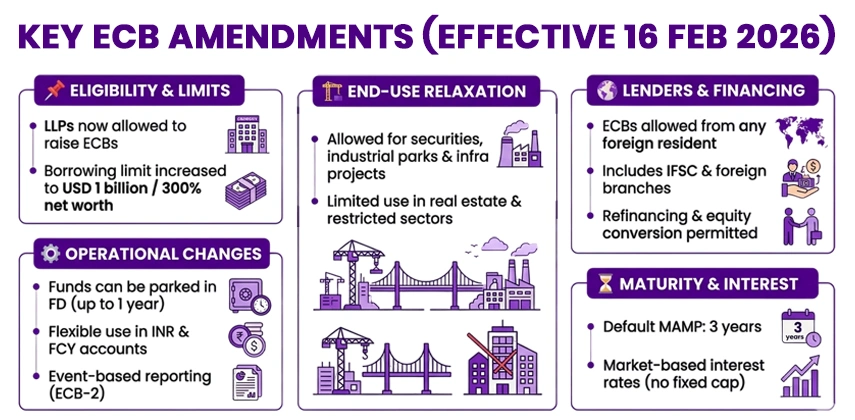

There are some amendments made by the RBI for ECBs through the Foreign Exchange Management Act, effective from 16th February, 2026. Here are the key amendments made by the Reserve Bank of India:

As per the amended RBI regulations, Limited Liability Partnerships (LLPs) can now avail ECBs. Companies under insolvency or restructuring can also borrow funds if their plan allows it. Additionally, even if a company is under investigation, it can still raise ECBs with proper disclosure.

Earlier, companies were allowed to borrow up to 750 million USD. However, this limit has now increased significantly, and a company can now borrow up to 1 billion USD or 300% of its net worth.

Funds can be temporarily kept in Fixed Deposits for up to 1 year. For INR expenses, proceeds must be transferred into an INR account in the next month. For FCY expenses, proceeds can be held in FCY accounts in India or abroad as allowed.

The end-use of ECBs is restricted for real estate and land-related activities, except where specifically permitted by RBI. ECBs can still not be used for most agricultural and plantation activities. However, these funds may now also be used for the following:

The earlier restriction (FATF/IOSCO countries) has been removed, offering more global funding options. ECBs can now be taken from any foreign resident, and foreign branches of RBI-regulated entities can also lend. Additionally, financial institutions in IFSCs are also allowed.

Existing ECBs can be refinanced, subject to original maturity rules. It can be converted into equity or non-debt instruments. Additionally, if a company is in financial trouble, restructuring rules will apply.

A uniform default MAMP of three years is established for all borrowers. However, manufacturing companies are allowed to raise ECBs with MAMP between 1-3 years, subject to the outstanding amount up to 150 million USD. Loans cannot be exited before completing this period.

There is no fixed cap now on ECBs, and the cost of borrowing is now determined based on the market-pricing. For ECBs with MAMP of less than three years, the cost of borrowing must adhere to trade credit pricing benchmarks.

Additionally, loans from related parties must follow arm's length pricing, which requires enhanced transfer pricing documentation.

Complying with the reporting requirement is not simplified. Monthly reporting has been removed with event-based reporting through Form ECB-2. Keep in mind that if the reporting is not done for four consecutive quarters, the borrower may be marked as 'untraceable'.

There are several advantages of ECBs, including:

Apart from all the benefits, there are some risks and disadvantages of External Commercial Borrowings, which are as follows:

For Non-resident Indians (NRIs), ECBs can play a vital role in financing cross-border business ventures. NRIs' involvement in startups, infrastructure projects, and international businesses operating between India and other countries is rapidly increasing. ECBs become a very useful funding option in many situations, including:

An NRI starting or investing in an Indian startup may raise ECBs. It can be raised from international lenders to fund business expansion, technology investment, or operational growth.

NRIs can also take part as overseas investors or lenders in certain financial arrangements. It allows them to support businesses in India while also earning returns on international lending structures.

Companies that have NRI shareholders may raise ECB funding to expand their operations. However, the companies must ensure that the borrowing structure adheres to the regulatory requirements and foreign investment guidelines.

NRIs running international businesses can raise ECBs to fund purchases, infrastructure projects, or expansion plans through their Indian subsidiaries.

External Commercial Borrowings provide access to competitive interest rates and significant fundraising opportunities. It allows Indian companies to access international capital for business growth and development. Although it offers several benefits, it also carries some challenges. Moreover, seeking assistance from an expert can help you understand everything about ECBs and their significance.

At Savetaxs, we are a team of experts who can help you access ECBs by ensuring you select the relevant route, have the required documents, and follow the steps accurately. Our team can guide you throughout the process to ensure you enjoy a hassle-free process. Contact us today and access ECBs easily to achieve sustainable economic growth and development.

Note: This guide is for information purposes only. The views expressed in this guide are personal and do not constitute the views of Savetaxs. Savetaxs or the author will not be responsible for any direct or indirect loss incurred by the reader for taking any decision based on the information or the contents. It is advisable to consult either a CA, CS, CPA or a professional tax expert from the Savetaxs team, as they are familiar with the current regulations and help you make accurate decisions and maintain accuracy throughout the whole process.

Mr Manish is a financial professional with over 10 years of experience in strategic financial planning, performance analysis, and compliance across different sectors, including Agriculture, Pharma, Manufacturing, & Oil and Gas. Mr Prajapati has a knack for managing financial accounts, driving business growth by optimizing cost efficiency and regulatory compliance. Additionally, he has expertise in developing financial models, preparing detailed cash flow statements, and closing the balance sheets.

Want to read more? Explore Blogs

_1772791127967.webp&w=828&q=75)

_1772887385012.webp&w=828&q=75)

_1773060834347.webp&w=828&q=75)

_1773060689892.webp&w=828&q=75)